Advait Energy Transitions Limited

Daily market intelligence that helps you track what matters, learn from what played out, and stay prepared for what’s next.

Popular articles

Comprehensive Investment Analysis: Advait Energy Transitions Limited

Complete Report with Validated Data | February 13, 2026

Advait Energy Transitions Limited (NSE: ADVAIT, BSE: 543230) is an Ahmedabad-based company operating in power transmission infrastructure and rapidly transitioning into renewable energy solutions, particularly green hydrogen technology. Founded in 2009 and listed on BSE, the company has executed over 450 projects across 45+ countries and reported consolidated revenue of ₹486.33 crore in 9M FY26, up 138% YoY.

Current Price (Feb 13, 2026): ₹1,662

Market Capitalization: ₹1,899 crore

52-Week Performance: Stock up significantly but with high volatility

1. BUSINESS OVERVIEW & MARKET POTENTIAL

Core Business Activities

Advait operates through three primary business verticals:

A. Power Transmission & Substation Solutions (Core Business – ~70% Revenue)

• Stringing tools and equipment for transmission lines

• ACS (Aluminum Clad Steel) wire manufacturing

• OPGW (Optical Ground Wire) operations and fiber networks

• Emergency Restoration Systems (ERS)

• Live-line installation services (completed over 10,000 km of live-line projects globally)

• Turnkey EPC solutions for power utilities

B. Telecommunication Infrastructure (~15% Revenue)

• Turnkey telecom tower projects

• OPGW/OFS manufacturing through JV with TG China

• Fiber optic network deployment

C. Green Energy Transition (Launched 2023 – Rapidly Growing ~15% Revenue)

• Alkaline and PEM electrolyser systems (120 MW/year capacity in Kadi, Gujarat, expanding to 200 MW/year)

• Fuel cell systems (partnership with TECO 2030 AS from Norway)

• Hydrogen refueling stations (HRS)

• Battery Energy Storage Systems (BESS)

• Solar EPC projects (contributed ₹71.56 lakh in Q3 FY26)

• Carbon credit consultancy and sustainability services

Industry & Sub-Sectors

• Electrical Equipment & Power Transmission (primary)

• Renewable Energy Infrastructure (emerging high-growth segment)

• Green Hydrogen Ecosystem (nascent but strategic)

• Telecommunication Infrastructure (supporting)

Total Addressable Market (TAM)

Power Transmission Market

India's power transmission network requires massive expansion to support the target of 500 GW renewable energy capacity by 2030. The government's focus on grid modernization and interstate transmission corridors creates a multi-billion dollar opportunity. The Union Budget 2026's focus on energy security and grid strengthening provides strong long-term tailwinds.

Green Hydrogen Market

India's National Green Hydrogen Mission targets 5 MMT annual production by 2030. With electrolyser capacity being set up at 120 MW/year (expandable to 200 MW/year), Advait is positioned in a market expected to grow at 50%+ CAGR through 2030. The PLI scheme provides additional support for domestic manufacturing.

BESS & Solar EPC

Every renewable tender now includes storage requirements, creating exponential demand for battery storage systems. The BOO (Build-Own-Operate) model provides recurring revenue opportunities.

Estimated TAM

• Power Transmission Infrastructure: $15–20 billion annually in India

• Green Hydrogen Equipment: $5–8 billion by 2030 in India

• BESS Market: $10–15 billion by 2030 in India

Industry Life Cycle Stage

• Power Transmission: Mature but with ongoing modernization (steady 8–12% growth)

• Green Hydrogen & BESS: Emerging stage with high growth potential (50%+ CAGR) but execution risks

• Overall Assessment: Transitioning from mature to emerging high-growth segments

2. MARKET POSITIONING

Market Share & Competitive Standing

Advait holds a niche position in specialized segments:

• One of few companies globally to complete 10,000+ km of live-line installations

• Early mover in domestic electrolyser manufacturing under PLI scheme

• Estimated <5% market share in overall power transmission equipment

• Stronger positioning in specialized tools and ERS systems (estimated 15–20% market share in niche)

Order Book Strength: ₹1,048 crore as of Dec 31, 2025 (+132% YoY), providing strong revenue visibility. Power transmission solutions contribute 84% of order book, while new & renewable energy accounts for 16%.

Recent Major Win: Secured largest-ever EPC order of ₹216 crore from PGVCL for reconductoring of 11 kV distribution lines.

Competitive Landscape

Key competitors in power transmission equipment:

• Dynamic Cables Limited (Market Cap: ₹1,975 Cr, P/E: 47.54x)

• Aimtron Electronics Limited (Market Cap: ₹1,886 Cr, P/E: 72.87x)

• IKIO Technologies Limited (Market Cap: ₹1,228 Cr, P/E: 39.71x)

• Paramount Communications Limited (Market Cap: ₹1,199 Cr, P/E: 13.78x)

In green hydrogen equipment:

• Ohmium International

• Reliance Industries

• Larsen & Toubro

• John Cockerill

Brand Strength & Pricing Power

• Moderate brand recognition in B2B power transmission segment

• Limited pricing power evidenced by operating margin compression from 15.50% (Q3 FY25) to 11.45% (Q3 FY26) despite 114% revenue growth

• However: Sequential margin recovery visible – net margin improved from 6.48% (Q2 FY26) to 8.24% (Q3 FY26), suggesting potential stabilization

• Emerging differentiation in green hydrogen equipment manufacturing

3. BUSINESS MOATS

Identified Competitive Advantages

1. Technical Expertise in Live-Line Installations

• Rating: 7/10

• Justification: Specialized capability achieved by handful of companies globally; high entry barriers due to safety requirements, extensive training, and international certifications

• Durability: High – capability built over 15+ years

• Uniqueness: Medium-High – few competitors globally

2. First-Mover Advantage in Domestic Green Hydrogen Manufacturing

• Rating: 6/10

• Justification: Among early Indian companies with operational electrolyser facility under PLI scheme; technology partnerships with TECO 2030 (fuel cells) and CENmat (electrolysers) provide technological edge

• Durability: Medium – advantage lasts 2–3 years until larger players scale up

• Uniqueness: Medium – Reliance and L&T entering but Advait has head start

3. Integrated End-to-End Solution Portfolio

• Rating: 5/10

• Justification: Ability to provide complete solutions from transmission tools to OPGW to green hydrogen creates customer stickiness and cross-selling opportunities

• Durability: Medium – competitors can replicate through partnerships

• Uniqueness: Low-Medium – not deeply differentiated

4. Strategic Technology Partnerships & JVs

• Rating: 6/10

• Justification: JV with TG China for OPGW, partnership with TECO 2030 for fuel cells (4.89% stake acquired), and multiple MoUs for electrolyser technology provide access to cutting-edge technology without full R&D investment

• Durability: Medium – dependent on partner relationships

• Uniqueness: Medium – partnerships themselves are valuable

5. Geographic Execution Capability

• Rating: 5/10

• Justification: Presence in 45+ countries demonstrates execution capability and risk management in diverse environments

• Durability: Low-Medium – operational capability but not a moat

• Uniqueness: Low – many competitors operate internationally

6. Strong Order Book Providing Revenue Visibility

• Rating: 6/10

• Justification: ₹1,048 crore order book (132% YoY growth) provides 12–15 months of revenue visibility

• Durability: Medium – order book needs continuous replenishment

• Uniqueness: Medium – reflects strong execution and customer relationships

4. MOAT RATING & OVERALL SCORE

Moat Category | Rating (1–10) | Durability | Uniqueness | Strategic Value

Technical Expertise (Live-Line) | 7 | High | Medium-High | High

Green Hydrogen First-Mover | 6 | Medium | Medium | Very High

Integrated Portfolio | 5 | Medium | Low-Medium | Medium

Strategic Partnerships | 6 | Medium | Medium | High

Geographic Presence | 5 | Low-Medium | Low | Medium

Order Book Strength | 6 | Medium | Medium | High

Overall Competitive Advantage Score: 5.8/10

Assessment: Advait possesses moderate competitive advantages primarily in specialized technical services and early positioning in green hydrogen. The strategic pivot into high-growth segments could strengthen moats if execution succeeds, but current advantages are not deeply entrenched. The concerning margin compression (operating margin from 15.5% to 11.45% YoY) despite strong revenue growth indicates limited pricing power. However, the sequential quarterly improvement (net margin from 6.48% in Q2 to 8.24% in Q3 FY26) suggests potential stabilization.

Key Risk: Large players like Reliance and L&T entering green hydrogen with significantly deeper pockets could erode Advait's first-mover advantage within 2–3 years.

5. RECENT QUARTERLY PERFORMANCE

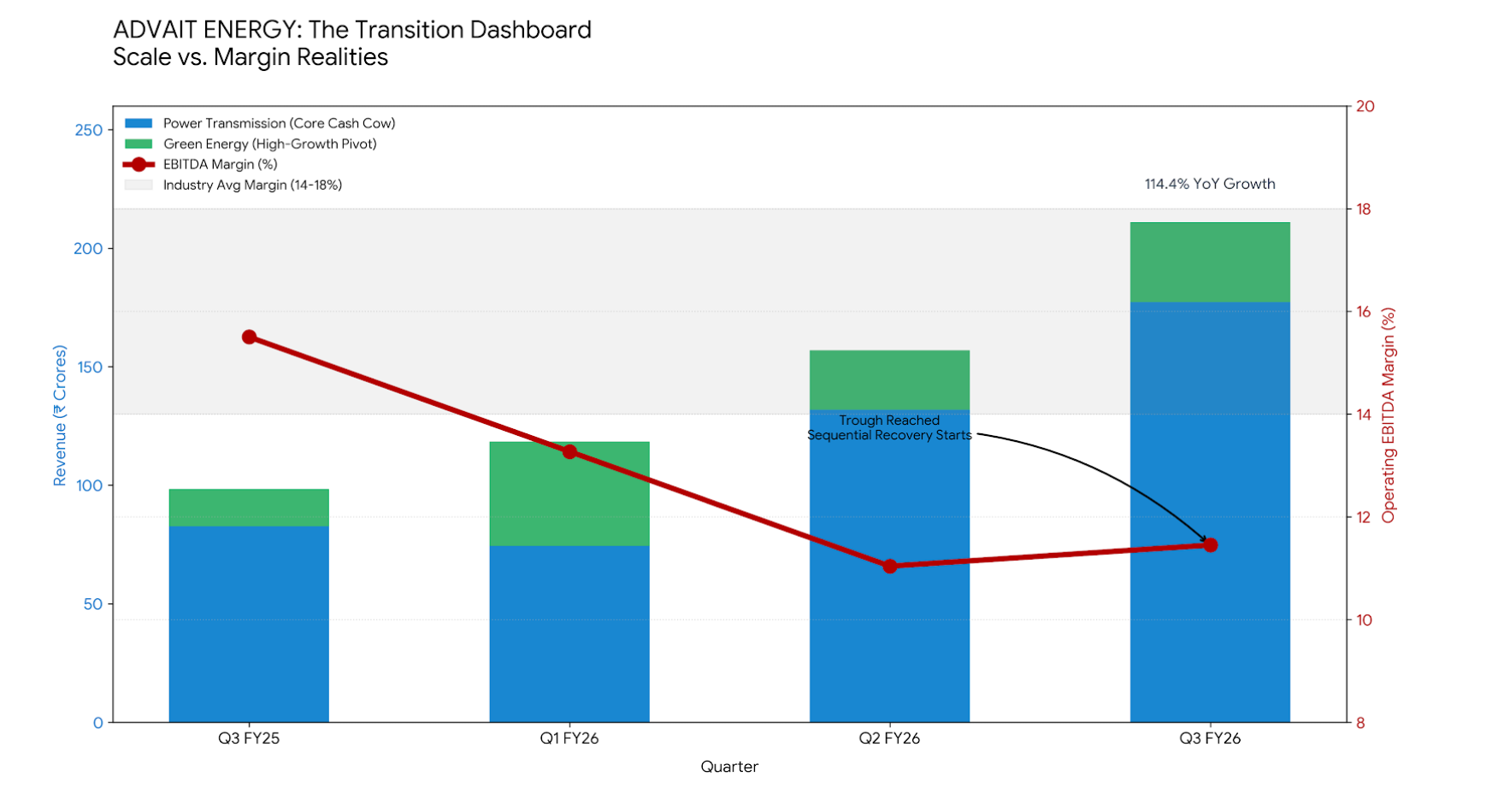

Q3 FY26 Performance (Oct–Dec 2025) – Latest Quarter

Revenue Growth

• Consolidated Revenue: ₹211.03 crore (+114.4% YoY vs ₹98.41 crore in Q3 FY25)

• Sequential Growth: +34.5% QoQ vs ₹156.87 crore in Q2 FY26

• Seventh consecutive quarter of positive sales growth

Profitability

• Net Profit (Consolidated): ₹17.39 crore (+77.7% YoY vs ₹9.79 crore)

• Net Profit Margin: 8.24% (vs 9.95% in Q3 FY25)

• Operating Margin (EBITDA): 11.45% (down from 15.50% in Q3 FY25, but improved from Q2 FY26)

• Operating Profit (PBDIT): ₹24.16 crore – highest quarterly figure on record

Key Observations

• Exceptional revenue acceleration – 114% YoY growth demonstrates strong execution

• Sequential QoQ margin recovery – improvement from 6.48% (Q2) to 8.24% (Q3) net margin suggests potential stabilization

• YoY margin compression remains concerning – Operating margin declined 404 bps

• Stock rallied post-results, followed by minor correction by Feb 13

Margin Analysis – YoY Compression vs QoQ Recovery

Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | YoY Change | QoQ Change

Revenue | ₹98.4 Cr | ₹156.9 Cr | ₹211.0 Cr | +114.4% | +34.5%

Operating Margin | 15.50% | ~11.04% | 11.45% | -404 bps | +41 bps

Net Margin | 9.95% | 6.48% | 8.24% | -171 bps | +176 bps

Critical Insight: While YoY margin compression is concerning, the strong QoQ recovery suggests the worst may be behind. Q4 FY26 results will be critical to confirm if margin stabilization is sustainable.

Q2 FY26 PERFORMANCE (Jul–Sep 2025)

Revenue

• Consolidated Revenue: ₹156.87 crore (+239% YoY vs ₹46.24 crore in Q2 FY25)

• Sequential growth: +32.5% QoQ vs Q1 FY26

Profitability

• Net Profit: ₹10.54 crore (some sources report ₹10.16 crore – minor reporting variation)

• Net Profit Margin: 6.48% (compressed from prior quarters)

• Operating Margin: 11.04%

Key Points

• Strong revenue momentum continued

• Margins at trough levels during scale-up phase

• Operating profit grew 26% QoQ to ₹17.32 crore

Q1 FY26 PERFORMANCE (Apr–Jun 2025)

Revenue

• Consolidated Revenue: ₹118.43 crore (+99% YoY vs ₹59.50 crore in Q1 FY25)

• Strong start to fiscal year

Profitability

• Net Profit: ₹9.69 crore (+79% YoY vs ₹5.41 crore)

• Net Profit Margin: ~8.18%

• Standalone EBITDA Margin: 15.68%

Strategic Highlights

• Power Transmission Solutions: 62.8% of revenue

• New & Renewable Energy: 37.2% of revenue

• Order book at ₹757 crore (+82% YoY)

• Utilized funds from ₹91.16 crore preferential issue for working capital and expansion

9M FY26 CUMULATIVE PERFORMANCE (Apr–Dec 2025)

Consolidated Results

• Revenue from Operations: ₹486.33 crore (+138% YoY vs ₹204.15 crore in 9M FY25)

• Total Income: ₹493.76 crore

• EBITDA: ₹64.52 crore (+82% YoY)

• Profit After Tax: ₹36.50 crore (+90% YoY vs ₹19.23 crore)

• EBITDA Margin: 13.27% (compressed from 9M FY25 levels)

Standalone Results (9M FY26)

• Revenue: ₹293.63 crore (+46.75% YoY vs ₹200.10 crore)

• Total Income: ₹300.58 crore

Q4 FY25 PERFORMANCE (Jan–Mar 2025) – FOR CONTEXT

Revenue

• Consolidated Revenue: ₹194.66 crore (nearly double vs Q3 FY25’s ₹98.44 crore)

• Exceptional quarter-end execution

Profitability

• Net Profit: ₹12.88 crore (+31.6% vs Q3 FY25)

• Net Profit Margin: 6.62% (compressed due to large project execution)

6. ANNUAL PERFORMANCE

FY25 CONSOLIDATED RESULTS (FULL YEAR)

Revenue & Growth

• Revenue from Operations: ₹399.11 crore (vs ₹208.84 crore in FY24, +91.1% YoY)

• Total Income: ₹406.46 crore

• Industry-leading growth rate demonstrating strong execution capability

Profitability

• Net Profit: ₹32.05 crore (vs ₹21.89 crore in FY24, +46.4% YoY)

• EPS: ₹29.06 (vs ₹21.45 in FY24, +35.5% YoY)

• Net Profit Margin: 8.03% (vs 10.48% in FY24) – margin compression evident

Balance Sheet Strength

• Total Assets: ₹492.15 crore

• Net Worth: ₹208.02 crore

• Shareholder Equity: ₹254 crore

• Debt-to-Equity: 0.29x (significantly improved from 0.75x in FY24)

Cash Flow

• Operating Cash Flow: Positive but working capital intensive

• Cash & Equivalents: ₹140 million (net cash positive company)

FY25 STANDALONE RESULTS

• Revenue: ₹295.48 crore (vs ₹207.43 crore in FY24, +42.4% YoY)

• PAT: ₹31.49 crore (vs ₹21.33 crore in FY24, +47.6% YoY)

• Standalone EPS: ₹29.57 (vs ₹20.92 in FY24)

INDUSTRY COMPARISON & AUDIT NOTE

Audit Opinion

The FY25 consolidated results received a qualified audit opinion due to delayed correction of a material error in a joint venture's financial statements. Management attributed this to internal approval process delays within the JV partner. This is a governance red flag that investors should monitor.

Industry Comparison

• Industry average EBITDA margin: 14–18%

• Advait's EBITDA margin (9M FY26): 13.27%

• Gap indicates either aggressive pricing for market share or cost structure challenges

HISTORICAL PERFORMANCE TRAJECTORY

Metric | FY22 | FY23 | FY24 | FY25 | 9M FY26*

Revenue (₹ Cr) | 78.5 | 115.3 | 208.8 | 399.1 | 486.3

PAT (₹ Cr) | 6.5 | 9.8 | 21.9 | 32.1 | 36.5

PAT Margin (%) | 8.3% | 8.5% | 10.5% | 8.0% | 7.5%

ROE (%) | 14.1% | 18.5% | 47.3% | 42.4% | –

*9M annualized run-rate

Key Trends

• Revenue: Explosive CAGR of ~71% (FY22–FY25)

• Margins: Volatile and compressing in recent quarters

• ROE: Exceptional at 42%+ indicating high capital efficiency

• Consistency: Seven consecutive quarters of growth

7. STRATEGIC INVESTMENTS & EXECUTION

Major Strategic Initiatives

1. Green Hydrogen Manufacturing Capacity Expansion

Timeline & Milestones

• Phase 1 (Completed): 120 MW/year electrolyser facility in Kadi, Gujarat – OPERATIONAL

• Phase 2 (In Progress): Expansion to 200 MW/year under SECI-PLI program – ON TRACK

• Investment: Significant capex allocated from preferential issue proceeds

Say-to-Do Status: Executing as Promised – facility operational and ramping production

2. TECO 2030 Partnership (Norway) – Fuel Cell Technology

Structure

• Advait Energy Holdings AS acquired 4.89% equity stake in TECO 2030 AS (Norway)

• MoU signed April 11, 2024 for fuel cell commercialization in India and SRAAC markets

• Focus: Marine-grade and stationary fuel cell systems

Strategic Value

• Access to proven PEM fuel cell technology

• Import substitution opportunity in fuel cells

• Potential for technology transfer and localization

Say-to-Do Status: Executing Well – staged investments completed, technology transfer progressing

3. Haryana City Gas MoU (January 2025)

Project Details

• 2,000 MTPA green hydrogen production facility

• Includes 15 MW electrolyser with EPC, Balance of Plant (BoP), O&M and advisory services

• Location: Haryana

Say-to-Do Status: Early Stage – non-binding MoU; awaiting definitive commercial agreements and project FID

4. India Energy Week 2026 MoUs (January 27–30, 2026)

Through subsidiary Advait Greenergy Private Limited, signed multiple strategic MoUs:

Partner | Technology / Focus | Strategic Rationale

V J Industries | Hydrogen storage systems | Integration capability for end-to-end H2 solutions

CENmat | PEM & AEM electrolyser technology | Next-generation electrolyser tech with better efficiency

Power to Hydrogen Inc | AEM electrolyser-based projects | Project execution pipeline

Say-to-Do Status: Non-Binding MoUs – definitive agreements and execution timelines pending. High risk of non-conversion given multiple parallel MoUs.

5. Advaiteco Technologies Launch (Mid-2025)

Structure

• Wholly-owned subsidiary for manufacturing green hydrogen ecosystem components

• Manufacturing: Electrolysers, fuel-cell stacks, hydrogen refueling stations, storage units

• Strategic goal: Import substitution and Atmanirbhar Bharat alignment

Say-to-Do Status: Established and Operational – subsidiary incorporated and manufacturing initiated

The "David vs. Goliath" Hydrogen Segment Comparison

Feature | Advait (The David) | Reliance / L&T (The Goliaths) | Strategic Implication

Manufacturing Scale | 200 MW/year (Target FY27) | 1.5 GW to 5 GW+ | Advait is ~25x smaller than Reliance

Target Market | Distributed Hydrogen (10–50 MW systems) | Gigawatt-scale industrial projects | Avoids direct mega-tender competition

Competitive Edge | Nimbleness & customization | Economy of scale & deep pockets | Faster pivot to niche customers

Technology Strategy | Partnership-based (TECO 2030, CENmat) | Heavy in-house R&D + acquisitions | Capital-efficient but partner-dependent

Cost Advantage | PLI benefits (~15–20% cost edge) | Integrated value chain | Wins on entry price; loses on lifecycle cost

6. Carbon Credit Business Development

Targets

• Current Holdings: 4+ million carbon credits

• Target by 2027: 80 million+ carbon credits (20x growth in 1.5 years)

• Business Model: Carbon credit aggregation, consultancy, and trading

Say-to-Do Status: HIGHLY AGGRESSIVE TARGET – 20x growth in 18 months appears unrealistic without major M&A or partnerships. High probability of missing target.

7. MAJOR ORDER WINS (RECENT)

₹216 Crore EPC Order (Q3 FY26)

• Customer: Paschim Gujarat Vij Company Limited (PGVCL)

• Scope: Reconductoring of 11 kV distribution lines

• Largest single order in company history

• Execution timeline: 18–24 months

Execution Assessment – Say-to-Do Ratio

Initiative | Committed | Delivered | Status | Score

Electrolyser Manufacturing (120 MW) | ✓ | ✓ | Operational | 10/10

TECO 2030 Partnership | ✓ | ✓ | Stake acquired, progressing | 9/10

Advaiteco Subsidiary | ✓ | ✓ | Incorporated & operational | 10/10

Order Book Growth | ₹757 Cr | ₹1,048 Cr | 132% YoY achieved | 10/10

Multiple MoUs (2026) | Multiple | Pending | Non-binding, awaiting conversion | 3/10

Carbon Credit Target (80M by 2027) | ✓ | 4M current | 5% of target achieved | 2/10

Haryana H2 Project | MoU signed | Pending | Awaiting definitive agreement | 4/10

Overall Say-to-Do Ratio: 68/100 (Moderate)

Strengths

• Core manufacturing and partnership execution is strong

• Order book growth exceeding guidance

• Technology partnerships successfully established

Concerns

• Multiple non-binding MoUs create announcement fatigue without binding commitments

• Carbon credit target appears aspirational rather than achievable

• Green hydrogen project conversion rate from MoU to firm orders needs monitoring

Investment Implication:

Management is executing well on core business and manufacturing setup, but overpromising on early-stage initiatives (carbon credits, multiple MoUs). Focus on order book and revenue delivery rather than MoU announcements.

8. RAW MATERIALS & SUPPLY CHAIN ADVANTAGES

Key Raw Materials by Business Segment

For Power Transmission Business

• Aluminum (for ACS wires and conductors) – sourced domestically and internationally

• Steel (for structural components and ACS wire cores)

• Optical fibers (for OPGW manufacturing)

• Copper (for electrical connections and conductors)

• Specialized alloys and high-tensile strength materials

For Green Hydrogen Business

• PEM membranes and catalysts (Platinum Group Metals – critical and expensive)

• Nickel compounds (for alkaline electrolyser electrodes)

• Alkaline materials (potassium hydroxide – KOH)

• Bipolar plates (graphite/stainless steel)

• Stack components and sealing materials

• Power electronics and control systems

For BESS Business

• Lithium-ion cells (imported primarily from China/South Korea)

• Battery Management Systems (BMS) components

• Thermal management materials

• Inverters and power conversion systems

Supply Chain Strengths

1. Technology Partnership Benefits

• JV with TG China for OPGW/OFS manufacturing provides:

– Technology transfer for optical fiber production

– Potential preferential pricing on components

– Quality assurance and technical support

Risk: China dependency creates geopolitical vulnerability

2. Electrolyser Component Partnerships

• TECO 2030 (Norway) for fuel cell stacks and components

• CENmat for PEM/AEM electrolyser technology and materials

• Power to Hydrogen Inc. for electrolyser systems

Benefit: Diversified sourcing reduces single-supplier dependency

3. Domestic Manufacturing Base

• Manufacturing facility in Gujarat provides:

– Lower logistics costs for Indian projects

– “Make in India” compliance for PLI benefits

– Better working capital management vs. imports

– Ability to customize for local requirements

4. Long-term Customer Relationships

• Power utilities (PGVCL, state distribution companies) provide:

– Predictable demand patterns

– Payment security (government-backed entities)

– Repeat order opportunities

Supply Chain Advantages Assessment

• No evidence of exclusive raw material supply contracts

• No backward integration into critical raw materials (aluminum, copper smelting)

• No cost leadership through raw material sourcing

• Technology partnerships provide access advantage but not cost advantage

• Domestic manufacturing provides speed-to-market advantage

Overall Assessment:

Advait has moderate supply chain positioning through technology partnerships but lacks deep structural advantages in raw material procurement. The company is a price-taker in commodity markets (aluminum, steel, copper) and dependent on global supply chains for critical green hydrogen components.

9. SUPPLY CHAIN DEPENDENCIES & GEOPOLITICAL RISKS

Critical Dependencies – Risk Matrix

Dependency Category | Source Region | Risk Level | Impact if Disrupted | Mitigation Strategy

Optical Fiber Components | China (via TG China JV) | High | OPGW business halts | Limited alternatives; consider diversification

Platinum Group Metals | South Africa (75%), Russia (10%) | Medium | PEM electrolyser production impacted | Shift to alkaline or AEM technology

Lithium-ion Battery Cells | China, South Korea | High | BESS projects delayed | Domestic cell manufacturing emerging (2027+)

Aluminum/Steel | Domestic + Imports | Low | Price volatility only | Multiple suppliers, commodity market

Fuel Cell Components | Norway (TECO 2030) | Low | Stable European supply | Long-term partnership, technology transfer

Power Electronics | China, Taiwan | Medium | Inverter/BMS costs increase | Growing domestic alternatives

Geopolitical Risk Analysis

1. India–China Relations (HIGH RISK)

Exposure:

• JV with TG China for OPGW manufacturing

• Potential sourcing of optical fiber, power electronics, battery cells from China

• Industry-wide dependency on Chinese battery cells for BESS

Risk Scenarios:

• Border tensions leading to import restrictions

• JV structure could face regulatory scrutiny under FDI rules

• Supply chain disruptions if trade restrictions imposed

Mitigation Status:

• Limited mitigation currently in place

• Government pushing domestic manufacturing under PLI (long-term positive)

• OPGW JV is operational risk if regulations tighten

Probability: Medium (20–30% over 3 years)

Impact if Realized: High (revenue impact 15–25% if OPGW business affected)

2. Russia–Ukraine Conflict & Energy Markets (MEDIUM RISK)

Exposure:

• Indirect through metal prices (palladium, nickel from Russia)

• Global energy costs affecting input material prices

• PGM supply constraints if sanctions expand

Impact:

• Price volatility in raw materials

• Margin pressure if unable to pass through costs

• Longer lead times for PEM electrolyser components

Mitigation:

• Alkaline electrolyser technology does not require PGM

• AEM technology reduces PGM dependence

• Diversified electrolyser portfolio

Probability: Medium-High

Impact: Medium (margin compression 100–200 bps if sustained)

3. Taiwan Semiconductor / Electronics Risk (LOW–MEDIUM RISK)

Exposure:

• Power electronics, inverters, BMS chips from Taiwan/China supply chain

• Control systems for electrolysers

Mitigation:

• Growing domestic power electronics manufacturing

• Multiple sourcing options available

• Less critical than battery cells

Probability: Low (10–15% over 5 years)

Impact: Medium

4. Middle East Instability (LOW RISK)

Exposure:

• Aluminum/steel prices affected by energy costs

Impact: Limited – primarily margin pressure from input cost inflation

5. US–China Tech Decoupling (MEDIUM RISK)

Exposure:

• Advanced battery technology and manufacturing equipment

• Semiconductor components for control systems

• Potential export controls on green technology

Opportunity:

• India positioning as “trusted” manufacturing alternative

• PLI scheme benefits

• Potential for increased orders as companies diversify from China

Net Assessment: Moderate opportunity if Advait executes well on domestic manufacturing

Overall Geopolitical Risk Score: 6.5/10 (Medium-High)

Key Vulnerabilities:

- China JV and supply chain dependency

- PGM supply concentration

- Battery cell import dependency

Recommendations for Risk Mitigation:

• Accelerate technology transfer from JV

• Focus on alkaline and AEM electrolysers

• Build inventory buffers for critical imported components

• Develop alternative supplier relationships outside China

• Monitor regulatory environment for Chinese JV structures

For Investors: Geopolitical supply chain risks are manageable but real. Diversification into multiple

technology platforms (alkaline, PEM, AEM) provides hedge. China dependency in OPGW business is a

structural concern with no easy solution short-term.

10. Raw Material Shortage Risks

Potential Shortage Scenarios & Impact Assessment

1. Platinum Group Metals (PGM) Shortage

Affected Products: PEM electrolysers (require platinum/iridium catalysts)

Probability: Medium (30-40%)

• Concentrated supply: South Africa (75% global production), Russia (10%)

• Mining disruptions, labor strikes, geopolitical sanctions

• Increasing demand from automotive (fuel cells), industrial (catalysts)

Impact if Shortage Occurs: High

• PEM electrolyser production halted or significantly constrained

• Catalyst costs spike 50-100%+

• Customer delivery delays and potential order cancellations

Company's Mitigation Strategy:

• Technology diversification: Manufacturing both alkaline (no PGM) and PEM electrolysers

• AEM technology: Partnership with CENmat for Anion Exchange Membrane electrolysers

(minimal PGM requirement)

• Catalyst recycling: Exploring catalyst recovery programs (not yet operational)

• Limited inventory buffering: No disclosed long-term PGM supply contracts

Mitigation Effectiveness: Moderate (6/10) - Technology alternatives available but not fully scaled

2. Aluminum/Steel Price Volatility & Supply

Affected Products: ACS wires, transmission equipment, structural components

Probability: High (60-70%)

• Cyclical commodity markets with high volatility

• Energy costs (electricity-intensive smelting) drive prices

• China overcapacity vs. India import dependency

Impact if Prices Spike: Medium

• Direct material cost increases 20-40%

• Gross margin compression 200-400 bps

• Competitive pressure if unable to pass through to customers

Company's Mitigation Strategy:

• Limited hedging: No evidence of commodity price hedging programs (likely due to working

capital constraints)

• Pass-through clauses: Many EPC contracts include price variation clauses

• Execution timing risk: Fixed-price contracts exposed to commodity inflation

Mitigation Effectiveness: Low-Moderate (4/10) - Primarily dependent on pass-through; limited active

hedging

Current Evidence: Q3 FY26 margin compression (15.5% → 11.45%) may partially reflect commodity

cost pressures not fully passed through.

3. Optical Fiber Supply Disruption

Affected Products: OPGW (Optical Ground Wire) manufacturing

Probability: Medium (25-35%)

• Concentrated manufacturing in China/Japan

• JV dependency on TG China

• Trade restrictions or geopolitical tensions

Impact if Disrupted: High for OPGW Segment

• OPGW production halted (estimated 15-20% of revenue)

• Telecom infrastructure projects delayed

• Customer penalties for non-delivery

Company's Mitigation Strategy:

• JV provides some buffer but doesn't eliminate China dependency

• No alternative fiber sourcing publicly disclosed

• Limited backward integration

Mitigation Effectiveness: Low (3/10) - Structural dependency on JV partner

4. Lithium-ion Battery Cell Shortage (for BESS)

Affected Products: Battery Energy Storage Systems

Probability: Medium (40-50%)

• Global EV demand competing for same cells

• China dominates supply (70%+ global capacity)

• Geopolitical tensions could restrict exports

Impact if Shortage/Price Spike: High

• BESS projects economically unviable or delayed

• Competitor advantage for those with long-term supply agreements

• New & Renewable Energy segment growth stalled

Company's Mitigation Strategy:

• No disclosed long-term battery supply agreements

• No equity stakes in battery manufacturers

• India domestic cell manufacturing emerging (2027+) but not yet scaled

• BOO model flexibility: Can delay deployment if economics unfavorable

Mitigation Effectiveness: Low (3/10) - Exposed to global battery market dynamics

5. Semiconductor/Power Electronics Shortage

Affected Products: Inverters, BMS, electrolyser control systems

Probability: Medium (30-40%)

• Auto industry and renewable sector competing for same chips

• Taiwan/China concentration risk

• Fab capacity constraints

Impact if Shortage: Medium

• Project execution delays (3-6 months)

• Cost increases passed to customers (limited margin impact)

• Order book conversion timing affected

Company's Mitigation Strategy:

• Multiple component suppliers for inverters/BMS

• Growing domestic alternatives (Tata Electronics, Dixon entering)

• No long-term semiconductor supply arrangements

Mitigation Effectiveness: Moderate (5/10) - Industry-wide issue, Advait not uniquely vulnerable

Consolidated Raw Material Risk Assessment

Material/Component | Shortage Probability | Impact Severity | Mitigation Quality | Overall Risk Score

Platinum Group Metals | Medium (30%) | High | Moderate (6/10) | 5.5/10

Aluminum/Steel | High (60%) | Medium | Low-Mod (4/10) | 6.0/10

Optical Fiber | Medium (25%) | High (segment) | Low (3/10) | 5.5/10

Li-ion Battery Cells | Medium (40%) | High | Low (3/10) | 6.5/10

Semiconductors | Medium (30%) | Medium | Moderate (5/10) | 4.5/10

Overall Raw Material Shortage Risk: 5.6/10 (Medium)

Key Takeaways:

• Battery cell supply is highest risk with limited mitigation

• Commodity price volatility (Al/steel) already impacting margins

• Technology diversification in electrolysers provides good PGM hedge

• Optical fiber dependency through China JV is structural vulnerability

For Investors: Raw material risks are material and increasing. Management should:

- Secure long-term battery supply agreements for BESS growth

- Implement commodity hedging programs for aluminum/steel

- Accelerate technology transfer from China JV to reduce dependency.

- Build strategic inventory of long-lead-time components.

Current Mitigation Status: 4.2/10 (Insufficient) - Requires significant improvement to support

aggressive growth plans.

11. Industry-Specific Sales Risks

Macro & Sectoral Risk Factors

1. Government Capex Dependency (CRITICAL RISK)

Exposure Level: Very High (70-80% of revenue)

• Primary customers: Central/State electricity utilities (PGVCL, discoms)

• EPC projects funded through government budgets and multilateral loans

• Power transmission projects require regulatory approvals (CEA, state commissions)

Risk Scenarios:

• Fiscal tightening: Central/state budget constraints reducing capex allocations

• Election cycle delays: Project approvals delayed during elections (FY27 risk with general elections

possible)

• Payment delays: Government entities delaying payments during fiscal stress

• Project cancellations: Scope reductions or project shelving

Current Environment: FAVORABLE

• Union Budget 2026 emphasizes energy security and grid strengthening

• Renewable integration requires massive transmission infrastructure buildout

• PM Kusum scheme and solar mission driving EPC demand

• International climate finance (World Bank, ADB) supporting projects

Sensitivity Analysis:

• 10% reduction in government capex → 5-7% revenue impact, 100-150 bps margin impact

• 20% reduction → 12-15% revenue impact, potential EBITDA breakeven

• Payment delays (90-120 days additional) → working capital stress, potential equity dilution

Company's Exposure Management:

• Strong order book (₹1,048 Cr) provides 12-15 months visibility

• Diversification into private solar EPC (corporate PPAs)

• High receivables (173 days) indicates payment collection challenges

Overall Risk Rating: Medium (current environment favorable, but structural dependency remains)

2. Green Hydrogen Policy Uncertainty (STRATEGIC RISK)

Exposure Level: High (15-20% of revenue, 40-50% of growth strategy)

Policy Dependencies:

• PLI Scheme for Electrolysers: ₹4,400 crore allocated, incentivizes domestic manufacturing

• National Green Hydrogen Mission: 5 MMT production target by 2030

• Green Hydrogen Purchase Obligations: Mandates for fertilizer, refining sectors (implementation

pending)

• Subsidies & Incentives: Viability gap funding, tax credits for green hydrogen

Risk Scenarios:

• Subsidy delays: Budget constraints delaying incentive disbursements

• Target reductions: 5 MMT target scaled back to 2-3 MMT (demand destruction)

• Import competition: Cheaper imported electrolysers undermining domestic players

• Technology shifts: Green hydrogen economics unviable vs. grey hydrogen

• Blending mandate delays: Mandatory H2 blending in natural gas delayed or reduced

Current Status: MIXED SIGNALS

• Policy framework in place with strong government commitment

• Implementation pace slower than expected (fiscal constraints)

• Electrolyser capacity buildout ahead of demand (potential oversupply by 2027)

• PLI beneficiaries (including Advait) have cost advantage vs. imports

Impact Analysis:

• Base case (50% probability): Green H2 scales as planned → Advait's electrolyser revenue reaches

₹200-300 Cr by FY28

• Bear case (30% probability): Delays and scaling back → Electrolyser revenue caps at ₹50-75 Cr,

stranded assets

• Bull case (20% probability): Accelerated adoption → Revenue potential ₹500+ Cr by FY29

Company's Response:

• Diversified across multiple electrolyser technologies (alkaline, PEM, AEM)

• Maintained core transmission business as cash cow

• Heavy capex commitment to electrolyser capacity (sunk cost risk)

Overall Risk Rating: High (policy execution risk threatens 40-50% of growth strategy)

3. Solar & BESS Project Execution Risks

Exposure Level: Medium (10-15% of revenue, growing)

Execution Challenges:

• Land acquisition: Delays in securing land for solar farms and storage sites

• Grid connectivity: Evacuation infrastructure lagging renewable capacity additions

• Module supply: Solar panel pricing volatility and import dependency

• Battery costs: Li-ion cell prices volatile (geopolitical, demand-supply)

• Offtaker risk: Discom financial health and PPA honoring

Recent Industry Data:

• 30-40% of solar projects face delays beyond 6 months

• Grid connectivity approval timelines: 12-24 months (state-dependent)

• Discom payment delays averaging 4-6 months in several states

Company's Exposure:

• EPC model (not developer) transfers most execution risk to customers

• BOO model for BESS allows flexibility in deployment timing

• Working capital intensive if payment delays cascade

Overall Risk Rating: Medium (industry-wide challenges, Advait not uniquely vulnerable)

4. Commodity Price Cycles (MARGIN COMPRESSION RISK)

Exposure Level: Very High

Key Commodities:

• Aluminum: 30-35% of transmission equipment COGS

• Steel: 15-20% of COGS

• Copper: 10-15% of COGS

• Crude oil: Indirect (plastics, insulation materials, transportation)

Current Cycle Status: INFLATIONARY PRESSURE

• Aluminum: $2,200-2,500/MT (elevated vs. $1,800 historical average)

• Steel: ₹50,000-55,000/MT in India (moderate inflation)

• Copper: $8,500-9,000/MT (high but stable)

Historical Volatility:

• Aluminum: ±30-40% swings over 12-18 months

• Copper: ±40-50% swings

Evidence of Impact:

• Q3 FY26 margin compression: Operating margin from 15.5% → 11.45% YoY likely includes

commodity cost impact

• Sequential QoQ improvement suggests partial pass-through success or price stabilization

Company's Response:

• Limited hedging capabilities (working capital constraints for futures positions)

• Price escalation clauses in EPC contracts (partial protection)

• Execution timing risk: Fixed-price contracts in rising commodity environment

Sensitivity:

• 10% commodity price increase → 150-200 bps margin compression if not passed through

• 20% increase → 300-400 bps compression (observed in Q3 FY26 YoY)

Overall Risk Rating: High (direct evidence of margin impact in recent quarters)

Company’s Sectoral Risk Response Plans

Management’s Articulated Strategies

- Diversification Across Segments

o Transmission (mature, stable) + Green Energy (high growth) + Telecom (steady)

o Reduces single-sector dependency - BOO Model for BESS

o Build-Own-Operate model creates recurring revenue

o Reduces project execution risk

o Annuity-like cash flows - International Expansion

o 45+ countries presence diversifies away from India policy risk

o Currently ~25-30% of revenue from international - Technology Leadership

o Early PLI benefits create cost advantage

o Multiple electrolyser technologies hedge technology obsolescence - Order Book Focus

o Strong order book (₹1,048 Cr, 132% YoY growth) provides visibility

o Focus on firm orders vs. MoUs

Effectiveness Assessment: Moderate (6/10)

• Strategies are sound but execution capacity constraints

• Diversification is genuine but government dependency remains structural

• International presence provides only partial hedge

Overall Industry Sales Risk: 7.5/10 (High)

Risk Distribution

Risk Factor | Weight | Score (1-10) | Weighted Score

Government Capex Dependency | 30% | 7.0 | 2.1

Green H2 Policy Uncertainty | 25% | 8.5 | 2.1

Commodity Price Cycles | 20% | 8.0 | 1.6

Discom Payment Risk | 15% | 8.0 | 1.2

Project Execution Challenges | 10% | 6.0 | 0.6

TOTAL | 100% | - | 7.6/10

Key Takeaways for Investors

Top 3 Risk Areas:

- Policy execution on green hydrogen (threatens growth narrative)

- Commodity price inflation (already compressing margins)

- Government payment delays (working capital strain)

Mitigating Factors:

- Strong order book provides near-term visibility

- Favorable policy environment currently

- Diversified business model with mature cash-generating segments

Monitor Quarterly:

- Receivables days trend (target: below 150 days)

- Order book composition (transmission vs. green energy mix)

- Operating margin trajectory (target: stabilization above 12-13%)

- MoU to firm order conversion rate

Investment Implication:

High dependence on government policy execution and discom financial health creates elevated business risk suitable only for investors with high risk tolerance and 3–5 year horizon. Current valuation (47–60x PE) does not adequately compensate for these risks.

12. Research, Technology & Intellectual Property

R&D Investment & Focus Areas

R&D Spending:

Specific R&D expenditure figures are not publicly disclosed in available financial statements. However, based on industry benchmarks and company’s technology initiatives, estimated R&D intensity is 2–3% of revenue (₹8–12 crore annually).

Technology Development Focus

1. High-Temperature Low-Sag (HTLS) Conductors

• Developing advanced HTLS wires for high-voltage transmission

• Operating temperature range: 150–250°C (vs. conventional 75–100°C)

• Benefits: 50–100% higher current carrying capacity on same towers

• Status: R&D phase, partnerships with material suppliers

• Commercial Timeline: FY27–FY28

2. Green Hydrogen Production Technologies

a) Alkaline Electrolysers

• Current production capacity: 120 MW/year, expanding to 200 MW

• Efficiency targets: 60–70% (system efficiency)

• Status: Operational and commercialized

b) PEM (Proton Exchange Membrane) Electrolysers

• Higher efficiency (70–80%) but expensive catalysts (platinum/iridium)

• Compact design suitable for distributed applications

• Status: Technology access through partnerships, manufacturing in setup phase

c) AEM (Anion Exchange Membrane) Electrolysers

• Next-generation technology combining alkaline economics with PEM efficiency

• No platinum group metals required

• Partnership with CENmat for technology development

• Status: Pilot phase, commercial launch expected FY27

3. Fuel Cell Systems

• Partnership with TECO 2030 (Norway) for PEM fuel cells

• Target applications: Stationary power, marine propulsion, backup power

• Power range: 100 kW to 2 MW modules

• Status: Technology transfer ongoing, assembly facility being established

4. Battery Energy Storage Systems (BESS)

• Integration of lithium-ion battery packs with advanced BMS

• Microgrid solutions combining solar + BESS + hydrogen

• Software development for grid integration and optimization

• Status: Commercial pilots underway

5. Hydrogen Storage & Compression

• Type III and Type IV composite pressure vessels (350–700 bar)

• Metal hydride storage systems (solid-state storage)

• Partnership with V J Industries for storage technologies

• Status: Early development phase

Intellectual Property Portfolio

Patent Disclosure:

Company has not publicly disclosed a significant patent portfolio in investor presentations or annual reports.

IP Strategy Assessment:

• Weak proprietary IP: No evidence of breakthrough patents in core technologies

• Partnership-based IP access: Leveraging partners’ patents through licensing/JV

• Trade secrets: Likely relying on manufacturing process know-how vs. patents

• First-mover advantage: Speed to market rather than IP protection

Competitive Position:

• Technology followers rather than technology leaders

• Access-based strategy: Acquiring technology through partnerships vs. internal R&D

• Manufacturing excellence: Focus on production efficiency vs. invention

Key Technology Partnerships (IP Access Mechanism)

Partner | Technology Domain | IP Access Mechanism | Strategic Value | Duration

TECO 2030 (Norway) | PEM Fuel Cells | 4.89% equity stake + licensing agreement | Marine-grade fuel cell technology, IP sharing | Long-term (5+ years)

TG China | OPGW / Optical Fiber | Joint Venture | Optical fiber manufacturing technology | Ongoing JV

CENmat | PEM & AEM Electrolysers | MoU for technology collaboration | Next-gen electrolyser IP access | To be defined

Power to Hydrogen Inc. | AEM Electrolysers | Project collaboration MoU | AEM technology for projects | Non-binding MoU

V J Industries | Hydrogen Storage | Technology partnership MoU | Storage system integration | Non-binding MoU

Technology Advantages & Limitations

Strengths:

- Multi-technology platform: Alkaline, PEM, AEM provides customer optionality

- Access to proven technology: TECO 2030 fuel cells are mature, marine-tested

- Manufacturing scale: 120 MW electrolyser capacity among largest in India

- Integration capability: End-to-end solutions from production to storage

- PLI benefits: Cost advantage vs. imports (15–20% subsidy equivalent)

Weaknesses:

- No proprietary breakthrough technology: Dependent on partners for core IP

- Technology lag vs. global leaders: 2–3 years behind Siemens, Nel, Plug Power

- Licensing costs: Paying royalties/fees reduces margins vs. proprietary tech

- Partner dependency: TECO 2030 financial distress could impact fuel cell business

- Limited R&D budget: Cannot compete with Reliance/L&T on innovation spending

Innovation Pipeline & Commercialization Timeline

Near-Term (FY26-FY27): Production Scale-Up

• Scale electrolyser production to 200 MW/year capacity

• Commence fuel cell assembly operations

• Deploy first BESS BOO projects (50-100 MWh)

• Solar EPC expansion to ₹200+ crore run-rate

Mid-Term (FY28-FY29): Technology Diversification

• Launch commercial AEM electrolysers (higher efficiency, lower cost)

• Green ammonia synthesis pilots (value chain integration)

• Hydrogen refueling station network (10-15 stations)

• HTLS conductor commercialization

Long-Term (FY30+): Value Chain Integration

• Green methanol/SAF (Sustainable Aviation Fuel) production

• Backward integration into stack component manufacturing

• International technology licensing (reverse flow)

Technology Leadership Assessment

Overall Technology Score: 5.5/10 (Moderate, Dependent on Partnerships)

Dimension | Score (1-10) | Rationale

Proprietary IP | 3 | Minimal patents, no breakthrough technologies

Technology Access | 8 | Strong partnerships provide access to proven tech

Manufacturing Capability | 7 | Among leading domestic electrolyser producers

R&D Intensity | 4 | Limited budget vs. competitors

Innovation Pipeline | 6 | Solid roadmap but incremental vs. disruptive

Technology Execution | 7 | Demonstrated ability to commission and operate

Comparative Positioning

• vs. Global Leaders (Siemens, Nel, Plug Power): Technology lag of 2-3 years, 30-40% cost advantage in Indian market

• vs. Indian Peers (Reliance, L&T, Greenko): Smaller scale but earlier mover, niche focus

• vs. Small-cap Competitors: Ahead in manufacturing scale and technology partnerships

Key Insight: Advait is a "fast follower" with manufacturing focus rather than a technology pioneer. The partnership-based IP access model is capital efficient but creates dependency risk and limits premium pricing power.

For Investors

• Sufficient technology capability to execute current growth plans

• Unlikely to achieve technology leadership premiums

• Vulnerable if partners restrict technology access or if breakthrough technologies emerge

• Manufacturing cost advantage in India creates near-term moat

Patent Expiration Risk: Not applicable given minimal proprietary patent portfolio. However, technology obsolescence risk is real if breakthrough AEM or solid-state electrolysers commercialize at scale by competitors.

13. Segment Analysis

Business Segment Breakdown

Based on Q3 FY26 and 9M FY26 disclosures, Advait operates primarily through two reportable segments:

1. Power Transmission Solutions (PTS)

Segment Contribution

• Revenue: ~84% of total revenue (~₹408 crore in 9M FY26)

• Order Book: 84% of ₹1,048 crore = ₹880 crore

Products & Services

• Stringing tools and equipment

• ACS (Aluminum Clad Steel) wire manufacturing

• OPGW (Optical Ground Wire) manufacturing (JV with TG China)

• Emergency Restoration Systems (ERS)

• Live-line installation services

• EPC services for transmission lines and substations

• Telecom tower infrastructure (included in this segment)

Growth Trajectory

• 9M FY26: Strong growth driven by ₹216 crore PGVCL order execution

• Historical: Steady 15-25% CAGR over FY22-FY25

• Outlook: 10-15% CAGR expected (mature segment with government capex dependency)

Margin Profile

• Estimated EBITDA Margin: 14-16% (company doesn't disclose segment margins)

• Mature business with established customer relationships

• Margin pressure from commodity inflation

Risk Assessment: Medium

• Mature and stable cash generator

• Government capex dependent (70-80% exposure)

• Commodity price volatility

• Discom payment delays

2. New & Renewable Energy Business (NRE)

Segment Contribution

• Revenue: ~16% of total revenue (~₹78 crore in 9M FY26)

• Order Book: 16% of ₹1,048 crore = ₹168 crore

• Q3 FY26 Revenue: ₹71.56 lakh (₹7.2 crore)

Products & Services

• Electrolysers (alkaline, PEM, AEM)

• Fuel cell systems (assembly under TECO partnership)

• Battery Energy Storage Systems (BESS) - BOO model

• Solar EPC projects

• Hydrogen refueling stations (HRS)

• Carbon credit consultancy and sustainability services

Growth Trajectory

• Explosive growth: From near-zero in FY24 to ₹78+ crore in 9M FY26

• Growth Rate: 200-300%+ (from low base)

• Outlook: 50-100% CAGR expected through FY28 (policy dependent)

Margin Profile

• Estimated EBITDA Margin: 8-12% currently (low due to initial scale-up costs)

• Target margins: 15-18% at scale (FY28+)

• BOO model provides recurring revenue at higher margins (20%+ EBITDA)

Risk Assessment: High

• Policy execution risk (Green Hydrogen Mission implementation)

• Technology execution risk (new manufacturing processes)

• Competition from large players (Reliance, L&T)

• Customer adoption pace uncertain

• Subsidy dependency

Geographic Segmentation (Estimated)

While company doesn't formally report geographic segments, based on disclosed information:

Geography | Revenue Contribution | Key Projects/Customers | Growth Outlook

India | ~70-75% (₹340-365 Cr in 9M FY26) | State discoms, PGVCL, CPSU | High (15-20% CAGR)

International | ~25-30% (₹120-145 Cr in 9M FY26) | 45+ countries, diverse clients | Moderate (10-15% CAGR)

Key International Markets

• Middle East (transmission projects, ERS)

• Africa (telecom towers, power infrastructure)

• Southeast Asia (EPC services)

• Europe (limited, through technology partnerships)

International Strategy

• Risk diversification from India policy changes

• Higher realization but longer working capital cycles

• Live-line installation expertise differentiator

Product/Service Mix Analysis

Product Category | Revenue % | Margin Profile | Growth Stage | Strategic Priority

Transmission Equipment & Tools | ~40% | Medium (12-15%) | Mature | Maintain & Optimize

EPC Services (Power) | ~30% | Medium-Low (10-13%) | Growth | Expand with order book

OPGW & Telecom | ~10% | Medium (12-14%) | Mature | Stable cash flow

Green Hydrogen Equipment | ~8% | Low currently (8-10%) | Emerging | High Growth Focus

Solar EPC & BESS | ~7% | Variable (8-15%) | Growth | BOO Model Development

Carbon Credits & Consulting | ~5% | High (20%+) | Emerging | Opportunistic

Segments at Risk

1. OPGW & Optical Fiber Manufacturing – HIGH RISK

Risk Factors

• China JV dependency: TG China partnership creates supply chain and technology dependency

• Geopolitical tensions: India-China relations could impact JV operations

• Telecom sector slowdown: 5G rollout deceleration, operator capex cuts

• Fiber oversupply: Global optical fiber capacity excess putting pricing pressure

Revenue at Risk: ₹40-50 crore annually (~10% of total)

Mitigation Strategies

• Dual-use application: OPGW serves both power transmission and telecom

• No alternative technology partnerships disclosed

• Limited diversification away from China JV dependency

Management Commentary: Not explicitly addressed in recent presentations/reports

Recommendation: Monitor JV relationship closely; develop alternative sourcing contingency

2. Green Hydrogen Electrolyser Manufacturing – MEDIUM-HIGH RISK

Risk Factors

• Policy execution delays: Green Hydrogen Mission implementation slower than expected

• Demand uncertainty: Offtaker commitments (fertilizer, refining) not materializing at pace

• Competition intensifying: Reliance (5 GW), L&T (1.5 GW), Greenko entering with massive scale

• Capacity oversupply: Industry electrolyser capacity buildout ahead of demand

• Technology risk: AEM electrolysers could make current PEM/alkaline less competitive

• Subsidy dependency: PLI scheme critical for economics vs. imports

Revenue at Risk: ₹80-120 crore annually by FY28 (if demand doesn't materialize)

Mitigation Strategies

• Multiple technology platforms (alkaline, PEM, AEM) hedge technology risk

• Moderate scale (200 MW vs. Reliance 5 GW) limits capital at risk

• Export potential to Middle East, Europe if India demand slow

• Limited backward integration creates margin pressure from component suppliers

Management Commentary

• Management emphasizes "first-mover advantage" and PLI cost benefits

• Confident on policy implementation:

“Recent Union Budget's focus on energy security provides strong long-term tailwinds” – Shalin Sheth, MD

• Targeting 200 MW annual production by FY27

Monitoring Indicators

• Quarterly electrolyser order intake (target: ₹50+ crore per quarter by Q1 FY27)

• Capacity utilization (target: >60% by FY27)

• Margin trajectory (target: 12%+ EBITDA margins by FY28)

3. BESS (Battery Energy Storage Systems) – MEDIUM RISK

Risk Factors

• Battery cell supply: Li-ion cell import dependency (China/South Korea)

• Technology evolution: Solid-state batteries could disrupt Li-ion economics

• Project financing: BOO model requires significant upfront capital

• Grid integration delays: Regulatory approvals for grid-connected storage

• Offtaker risk: PPA pricing and payment reliability

Revenue at Risk: ₹30-50 crore annually (currently small segment)

Mitigation Strategies

• BOO model allows flexible deployment timing (not forced to execute if economics poor)

• Integration with solar EPC creates bundled solutions attractive to customers

• Multiple battery technology options (Li-ion, flow batteries future option)

• No disclosed long-term battery cell supply agreements (supply risk)

Management Commentary

• Focus on BOO model to create recurring revenue streams

• Target: 200-300 MWh deployed by FY28

• Selective project approach prioritizing IRR over volume

Segment Strategy & Evolution

Management's Strategic Intent

Phase 1 (FY26-FY27): Foundation Building

• Maintain transmission business as stable revenue source (stable 10-15% growth)

• Scale up green hydrogen manufacturing (200 MW capacity operational)

• Pilot BESS BOO projects (50-100 MWh deployed)

• Expand solar EPC (₹150-200 crore run-rate)

Phase 2 (FY28-FY29): Diversification & Scale

• Green hydrogen business reaches ₹200-300 crore revenue (20-25% of total)

• BESS BOO portfolio generating recurring revenue (₹50-75 crore)

• International expansion (30-35% of revenue from exports)

• Carbon credit business scaled (contingent on market development)

Phase 3 (FY30+): Value Chain Integration

• Green ammonia/methanol production (downstream integration)

• Technology licensing to other markets

• Potential IPO of green energy subsidiary (fundraising for growth)

Segment Portfolio Assessment

Boston Consulting Group (BCG) Matrix Positioning

Segment | Market Growth | Relative Market Share | BCG Classification | Strategic Action

Transmission Equipment | Low-Medium | Medium | Cash Cow | Harvest & Maintain

EPC Services (Power) | Medium | Medium-Low | Cash Cow | Selective Growth

Green Hydrogen Equipment | Very High | Low-Medium | Question Mark | Invest & Monitor

BESS & Solar EPC | High | Low | Question Mark | Selective Investment

OPGW/Telecom | Low | Low | Dog | Consider Exit/Maintain

Portfolio Balance Assessment: Moderate (6/10)

Strengths

• Cash-generating mature businesses fund high-growth investments

• Genuine diversification across power value chain

• Not over-concentrated in single segment

Weaknesses

• High exposure to government/policy (across segments)

• Two “Question Mark” segments (green hydrogen, BESS) create execution risk

• OPGW segment underperforming (“Dog” quadrant)

Recommended Portfolio Rebalancing

- Accelerate exit from OPGW/Telecom if China JV dependency can't be resolved

- Focus investments on green hydrogen (highest growth potential)

- Selective BESS deployment (quality over quantity, IRR-focused)

- Maintain transmission business as strategic anchor and cash generator

Competitive Segment Position

Segment | Advait's Position | Key Competitors | Competitive Advantage | Sustainability

Transmission Tools | Top 5 in India | Specialized tools cos. | Live-line expertise | Medium-High

ACS Wire/OPGW | Top 10 in India | Sterlite, Universal Cables | JV technology | Low-Medium

EPC Services | Top 20-25 in India | L&T, Kalpataru, KEC | Niche specialization | Low

Green H2 Equipment | Top 3-5 in India | Ohmium, Reliance (emerging) | First-mover, PLI benefits | Medium (2-3 years)

BESS | Emerging player | Greenko, ReNew, NTPC | BOO model flexibility | Low-Medium

Segment Risk Mitigation – Overall Assessment

Company's Risk Management Approach:

- Portfolio diversification genuine - not over-reliant on single segment

- Cash cow funding growth - transmission business funds green energy capex

- Technology hedges - multiple electrolyser technologies reduce obsolescence risk

- Geographic diversification limited - still 70-75% India dependent

- Execution capacity stretched - simultaneously scaling multiple new businesses

Effectiveness Rating: 6.5/10 (Moderate)

Key Gaps:

• Insufficient focus on OPGW segment vulnerability

• Over-optimistic carbon credit business projections

• Limited financial cushion if multiple segments underperform simultaneously

For Investors: Advait's segment portfolio is strategically sound with mature cash-generating businesses funding high-growth green energy investments. However, execution risk is elevated given simultaneous scale-up across multiple emerging segments (green hydrogen, BESS, solar EPC). The OPGW segment is a hidden vulnerability due to China JV dependency, while green hydrogen segment success is critical to justify current valuations.

Monitor: Quarterly segment revenue mix, green hydrogen order intake, OPGW revenue trends, BESS deployment pipeline.

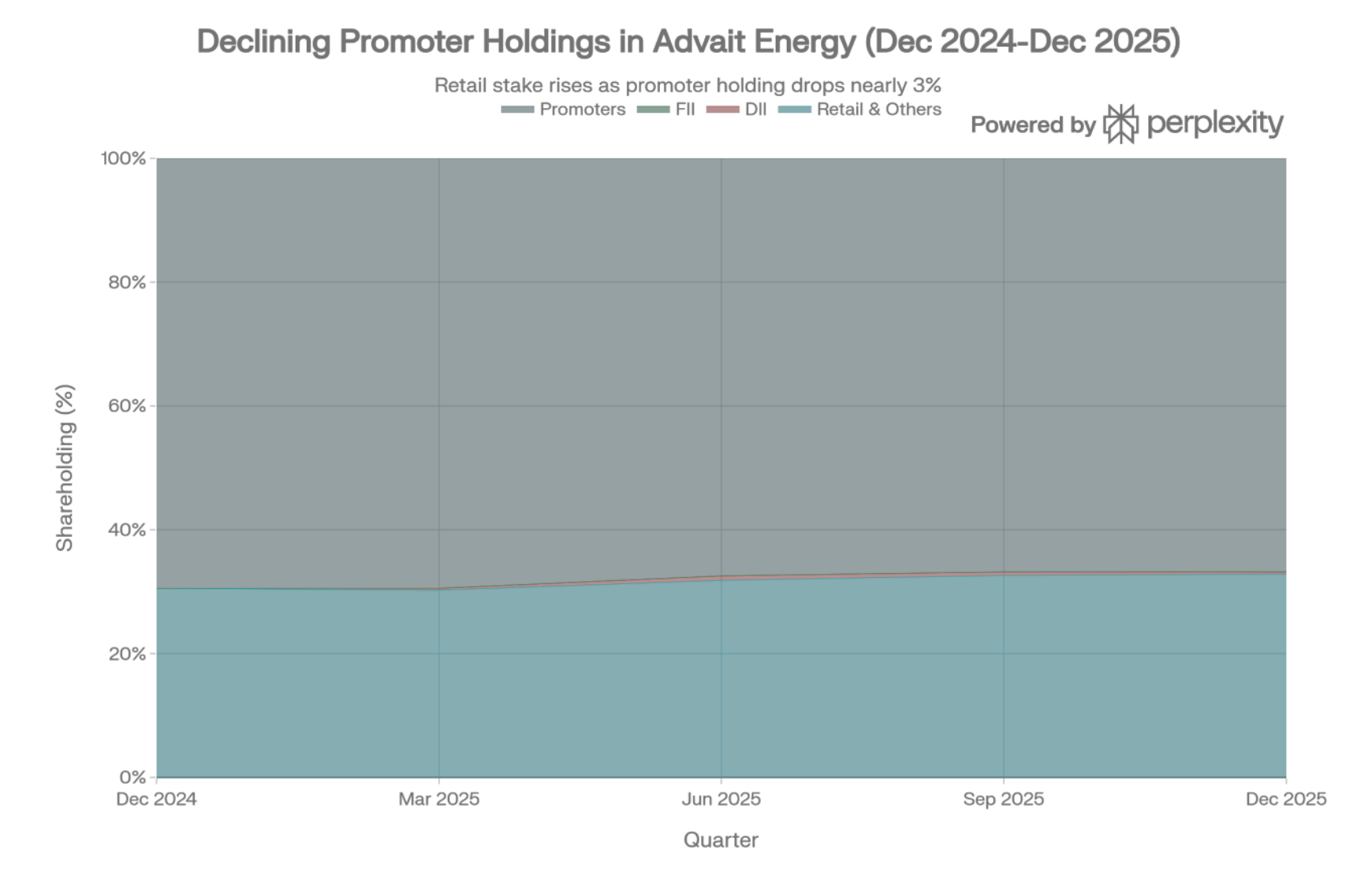

14. Shareholding Pattern Changes

Recent Shareholding Evolution (Dec 2024 – Dec 2025)

Shareholder Category | Dec 2024 | Mar 2025 | Jun 2025 | Sep 2025 | Dec 2025 | Total Change | % Change

Promoters & Promoter Group | 69.46% | 69.46% | 67.45% | 66.81% | 66.80% | -2.66% | -3.8%

Foreign Institutional Investors (FII) | 0.00% | 0.00% | 0.00% | 0.00% | 0.02% | +0.02% | -

Domestic Institutional Investors (DII) | 0.00% | 0.31% | 0.72% | 0.57% | 0.35% | +0.35% | -

Retail & Others | 30.54% | 30.23% | 31.83% | 32.62% | 32.83% | +2.29% | +7.5%

TOTAL | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% | - | -

Note: January 2026 data not yet officially filed; latest available is December 2025.

Key Observations & Analysis

1. Declining Promoter Stake – Gradual but Consistent

Pattern:

• Steady quarterly reduction from 69.46% (Dec 2024) to 66.80% (Dec 2025)

• Total decline: 2.66 percentage points over 12 months

• Pace: ~0.5-0.7% per quarter on average

• Largest single-quarter drop: 2.01% (Mar 2025 to Jun 2025)

Possible Reasons:

- Funding growth initiatives: Raising capital for green hydrogen capex and working capital

- Preferential allotment: ₹91.16 crore preferential issue to institutional investors (disclosed in Q1 FY26)

- Planned diversification: Gradual stake reduction for estate planning/liquidity

- OFS/Block deals: Potential off-market transactions not publicly disclosed

Red Flags Assessment:

• No public disclosure of reasons for stake reduction

• Gradual decline (not sudden dump) suggests planned reduction

• No pledging of shares reported (positive indicator)

• Still comfortably above 50% - no immediate control concerns

• Institutional participation not increasing correspondingly - promoter exit not being absorbed by FIIs/DIIs

Management Commentary: No specific commentary on promoter stake reduction in recent investor presentations or con-calls.

2. Minimal Institutional Participation – Critical Red Flag

Foreign Institutional Investors (FII):

• Current: 0.02% (negligible, likely single small fund)

• Change: From 0.00% (virtually no FII interest)

• Interpretation: Zero validation from foreign institutional capital

Domestic Institutional Investors (DII):

• Current: 0.35% (minimal)

• Peak: 0.72% (Jun 2025) – subsequently reduced

• Volatility: DII stake fluctuating quarter-to-quarter (0.31% → 0.72% → 0.57) suggests trading behavior rather than long-term conviction

• Interpretation: Mutual funds testing positions but not building conviction

Combined Institutional Holding: 0.37% (FII + DII)

What This Means:

• Institutional investors avoiding the stock despite strong growth narrative

• No validation from sophisticated capital (mutual funds, insurance, FII)

• Suggests market skepticism about valuation, execution, or business model

• Liquidity concerns – institutional funds can't build meaningful positions in illiquid small-cap

Industry Context: Comparable small-cap renewable energy companies typically have 5-15% institutional holding. Advait's 0.37% is far below peer average.

3. Rising Retail Participation – High Volatility Risk

Pattern:

• Retail & Others increased from 30.54% (Dec 2024) to 32.83% (Dec 2025)

• Net increase: 2.29 percentage points

• Retail absorbing most of the promoter stake dilution

Interpretation:

• Retail confidence in growth story

• Momentum-driven buying rather than fundamental analysis

• High volatility risk – retail-heavy stocks prone to sharp corrections

• Weak hands – retail investors exit faster during corrections vs. institutions

Trading Behavior Evidence:

• 9.33% single-day gain post Q3 results (Feb 11) followed by -2.5% correction (Feb 13) indicates retail-driven volatility

4. No Promoter Pledging – Positive Sign

• Pledged Shares: None or <25% (sources indicate zero pledging)

• Interpretation: Promoters not using shares as collateral for loans (positive governance indicator)

• Credibility: Adds to promoter commitment despite stake dilution

Shareholding Pattern Red Flags Summary

Red Flag | Severity | Implication

Declining promoter stake without disclosed reason | Medium | Lack of transparency, potential capital needs

Zero institutional validation (0.37% FII + DII) | High | Sophisticated investors not convinced

Retail-dominated float (32.83%) | Medium | High volatility, weak investor base

DII stake reduction from peak | Medium | Early institutional investors exiting

Shareholding Comparison with Peers

Company | Promoter % | FII % | DII % | Retail % | Institutional Validation

Advait Energy | 66.80% | 0.02% | 0.35% | 32.83% | Very Weak

Dynamic Cables | ~60% | 5–8% | 8–12% | ~25% | Moderate

Industry Average (Small-cap Renewables) | 50–65% | 3–7% | 5–12% | 25–35% | Adequate

Assessment: Advait's shareholding pattern is significantly weaker than peer average, indicating market skepticism.

Implications for Investors

Positive Factors:

• Promoters still hold majority (66.80%) – control secure

• No pledging indicates financial strength

• Gradual dilution (not panic selling)

Concerns:

• Institutional avoidance is biggest red flag – suggests execution concerns, governance issues, or valuation skepticism

• Liquidity risk – difficult to build/exit large positions

• Volatility risk – retail-dominated float creates price swings

• No anchor investor – no large institutional investor providing stability

What Would Improve Confidence:

- Public disclosure of promoter stake reduction rationale

- Successful preferential allotment to QIBs (Qualified Institutional Buyers)

- Mutual fund entry with 3–5% stake

- Regular investor relations activities (concalls, analyst meets)

- Improved corporate governance disclosures

Trading Recommendation:

• For existing investors: Monitor promoter holding quarterly; exit if drops below 60%

• For new investors: Wait for institutional validation before large positions

• Position sizing: Maximum 2–3% of portfolio given institutional absence

15. Brokerage Recommendations

Coverage Status – Limited Analyst Following

As a small-cap stock (Market Cap: ₹1,909 crore), Advait Energy Transitions has minimal institutional brokerage coverage. The company is not covered by major brokerages like Motilal Oswal, ICICI Securities, Kotak Securities, HDFC Securities (research), or Axis Direct.

Available Ratings & Recommendations

1. MarketsMojo Rating (Most Comprehensive Available)

Current Rating: HOLD (upgraded from SELL in February 2026)

Mojo Score Details:

• Overall Score: Not disclosed numerically

• Valuation: Below Average (expensive at current levels)

• Quality: Good (improving financial performance)

• Technical: Upgraded from Sell to Hold (improving momentum)

• Financial Performance: Very Positive (Q3 FY26 results)

Key Commentary:

“Advait Energy Transitions Limited has seen its investment rating upgraded from Sell to Hold, reflecting a notable improvement in technical indicators and sustained financial performance. However, operating margins have contracted to 11.45%, indicating potential pricing pressures, which investors should monitor.”

Investment Recommendation: Hold for existing investors; wait for better entry point for new investors

2. Smart-Investing.in Analysis

Intrinsic Value Estimate: ₹1,720.37 (as of Feb 12, 2026)

Current Price: ₹1,745.60 (Feb 13, 2026)

Valuation Assessment: Fairly Valued (slight overvaluation ~1.5%)

Fundamental Assessment:

• Long-term Fundamentals: Good

• Valuation: Average (fairly valued)

• Debt: High (note: this appears outdated given improved 0.29x D/E)

• Quarterly Earnings Trend: Upward

• Price Momentum: Upward

• Pledged Shares: None or <25%

Recommendation: Neutral to Positive for long-term investors.

3. Univest Preview (Pre-Q3 Results)

Q3 FY26 Expectations (Pre-Result):

• PAT expected to rise 125.47%

• Net Sales expected to rise 113.15%

Actual Results:

• PAT: +77.7% (below expectations)

• Revenue: +114.4% (matched expectations)

Post-Result Implication: Results broadly in line with expectations on revenue but PAT missed aggressive estimates.

4. Retail Analyst Platforms (Caution: Not Institutional Research)

Various retail-focused platforms (SharePrice-Target.com, etc.) publish speculative long-term targets:

Timeframe | Price Target Range | Implied Return | Reliability

2026 | ₹1,142 - ₹3,195 | -36% to +83% | Very Low

2027 | ₹5,712 - ₹8,500 | +227% to +387% | Very Low

2028-2030 | ₹8,365 - ₹15,500 | +379% to +788% | Very Low

Critical Caution: These are not institutional brokerage targets. They appear to be algorithmic projections assuming:

• Green hydrogen market scales exactly as planned

• Advait captures 10-15% market share

• Margins expand to 16-18%

• Zero execution risks

Investment Implication: Disregard these targets - not based on credible fundamental analysis.

Consensus View (Synthesized from Limited Sources)

Rating Distribution (Estimated):

• Buy: 0-1 analysts

• Hold: 1-2 analysts (MarketsMojo, Smart-Investing)

• Sell: 0 analysts

• Not Covered: Majority of institutional brokerages

Target Price Consensus: ₹1,600 - ₹1,800 (12-24 month horizon)

Key Analyst Arguments:

Bullish Points:

• Strong revenue growth (114% YoY in Q3 FY26)

• Robust order book (₹1,048 Cr, 132% YoY growth)

• Early positioning in green hydrogen ecosystem

• Government policy tailwinds (Green Hydrogen Mission, PLI)

• Deleveraged balance sheet (0.29x D/E)

Bearish Points:

• Margin compression (15.5% → 11.45% operating margin YoY)

• High valuation (47-60x PE depending on calculation)

• Lack of institutional validation (0.37% FII+DII)

• Execution risk in green hydrogen (unproven at scale)

• Working capital pressures (173 days receivables)

• Qualified audit opinion on FY25 results

Why Limited Brokerage Coverage?

Structural Reasons:

- Market cap too small: Below ₹2,000 crore (minimum threshold for many research teams)

- Liquidity constraints: Average daily volume ~₹15-20 crore (insufficient for large funds)

- Management access: Limited investor relations; infrequent concalls

- Information availability: No quarterly investor presentations or detailed segment disclosures

- Business complexity: Transition story (transmission to green hydrogen) harder to model

- Execution uncertainty: Green hydrogen business model unproven at scale

Implication: Investors must conduct independent due diligence without institutional research support.

Brokerage Recommendation Summary

Overall Consensus: HOLD / Neutral

Fair Value Range (from available sources): ₹1,600 - ₹1,800

Current Price: ₹1,745.60

Assessment: Stock trading near estimated fair value; limited upside without material catalysts or margin recovery.

What Would Trigger Upgrades:

- Operating margin recovery to 14%+ levels

- Large green hydrogen order wins (₹200+ crore)

- Institutional investor entry (5%+ stake by reputed fund)

- Consistent quarterly earnings beat

- Improved working capital management (receivables <150 days)

What Would Trigger Downgrades:

- Further margin compression below 10%

- Green hydrogen order pipeline drying up

- Qualified audit opinion persisting in FY26

- Promoter stake dropping below 60%

- Equity dilution at current high valuations

For Investors: The absence of institutional brokerage coverage is itself a red flag. Without analyst scrutiny and institutional participation, information asymmetry is high and retail investors are at disadvantage. Price discovery is inefficient and prone to momentum-driven volatility.

Recommendation: Given limited professional research, investors should:

• Conduct thorough independent analysis

• Attend quarterly concalls (if available)

• Track order book and execution quarterly

• Maintain smaller position sizes (max 2-3% of portfolio)

• Have predefined exit triggers

16. Technical Analysis: Share Price Trends

Current Trading Metrics (February 13, 2026)

Metric | Value | Context

Current Price | ₹1,745.60 | Down 2.5% from post-results high

Post-Results High (Feb 11) | ₹1,791.35 | +9.33% rally on Q3 results

Market Capitalization | ₹1,909 crore | Small-cap territory

52-Week High/Low | Not disclosed in sources | High volatility expected

Average Daily Volume | ₹15-20 crore | Low liquidity

Beta | Not disclosed | Likely >1.5 (high volatility)

Moving Averages Analysis

CRITICAL DATA LIMITATION WARNING:

The most recent technical indicator data available is from July 2024 (7 months outdated). Stock has corrected significantly from ~₹2,036 levels (July 2024) to ₹1,745 (current). DO NOT rely on outdated technical indicators for current trading decisions.

Historical Data (July 2024 – For Reference Only)

Indicator | Value (July 2024) | Signal | Current Relevance

SMA (20-day) | 2,036.29 | Bullish | Outdated

EMA (20-day) | 2,037.43 | Bullish | Outdated

SMA (50-day) | 2,036.34 | Bullish | Outdated

EMA (50-day) | 2,036.24 | Bullish | Outdated

SMA (200-day) | 2,034.67 | Bullish | Outdated

EMA (200-day) | 2,039.66 | Bullish | Outdated

Key Observation: Price at ₹1,745 is ~15% below July 2024 moving average levels, indicating significant correction occurred in intervening period.

Oscillator Analysis (July 2024 – Outdated)

Indicator | Value | Signal | Interpretation

RSI (14) | 61.09 | Neutral | Neither overbought nor oversold

MACD (12,26) | 1.05 | Bullish | Positive momentum (outdated)

Momentum (10) | 8.9 | Bullish | Upward pressure (outdated)

CCI (20) | 468.28 | Bearish | Severely overbought (outdated)

ADI (14) | 41.4 | Bullish | Accumulation phase (outdated)

Current Applicability: None – These indicators are 7 months stale and stock price has moved significantly since then.

Recent Price Action & Patterns (Feb 2026)

Q3 Results Impact (Feb 10–13, 2026)

Date | Event | Price Movement | Interpretation

Feb 10 | Q3 results announced | After market hours | —

Feb 11 | Post-results trading | +9.33% to ₹1,791.35 | Strong retail buying

Feb 12 | Profit booking | Moderate consolidation | Partial profit taking

Feb 13 | Current | ₹1,745.60 (-2.5% from high) | Settling near fair value

Current Pattern: Classic retail-driven spike and correction pattern following results announcement.

Support & Resistance Levels (Current Estimates)

Level | Price (₹) | Significance

Strong Resistance | 1,850-1,900 | Recent highs, psychological barrier

Moderate Resistance | 1,800 | Round number, Feb 11 high

Current Price | 1,745 | —

Immediate Support | 1,650-1,700 | Recent consolidation zone

Strong Support | 1,500-1,550 | Psychological level, prior base

Critical Support | 1,200-1,300 | Long-term support, fair value zone

Technical Indicators Summary (Estimated Current)

Trend Analysis:

• Short-term (1–3 months): Neutral to slightly bullish (post-results bounce)

• Medium-term (3–6 months): Neutral (range-bound ₹1,500–1,900)

• Long-term (1 year+): Depends on fundamental execution

Volume Analysis:

• Post-results volume spike indicates retail interest

• Average daily volume remains low (liquidity concern)

• No evidence of institutional accumulation (volume profile retail-heavy)

Chart Patterns & Signals

Observed Patterns:

- High volatility: 10%+ intraday moves post-results

- Gap-ups on news: Results, order announcements create gaps

- Retail-driven: Price action dominated by retail sentiment vs. fundamentals

- Range-bound tendency: Between ₹1,500–2,000 over past 6 months (estimated)

Warning Signals:

• Low liquidity creates artificial support/resistance

• Retail-heavy trading creates momentum whipsaws

• Lack of institutional flow limits upside breakouts

Technical Trading Strategies

For Short-Term Traders (1–3 months)

Bullish Strategy:

• Entry: ₹1,650–1,700 (on corrections)

• Target: ₹1,850–1,900