March 16, 2026 | Bearish Marubozu Signals Continued Downtrend as FII Selling Accelerates and 23,000 Emerges as Critical Support

Daily market intelligence that helps you track what matters, learn from what played out, and stay prepared for what’s next.

Popular articles

90-SECOND SUMMARY

The aircraft is still descending. Nifty closed at 23,151 on Friday — a bearish marubozu with no upper shadow, marking a -5.31% WoW loss, the worst week of 2026. FII sold aggressively on all 5 days, peaking at ₹10,717 Cr on Friday, while DIIs absorbed 99.93% of that outflow. The market enters Monday sitting 349 points below max pain (23,500), with VIX at 22.65 — the floor ratcheting higher for the 4th straight week.

TERM OF THE DAY

Bearish Marubozu — A candlestick with no upper shadow and a minimal lower shadow. Open ≈ High; Close ≈ Low. It signals relentless selling from open to close with zero buying recovery. Friday's Nifty (O: 23,463 → C: 23,151) is textbook. In trending markets, a bearish marubozu is not a reversal signal — it is a continuation pattern until proven otherwise.

MARKET SNAPSHOT — CLOSE 13-MAR-2026

Index | Close | Chg % | Open | High | Low | 52W High | 52W Low | PE

Nifty 50 | 23,151 | -2.06 | 23,463 | 23,492 | 23,112 | 26,373 | 21,744 | 20.26x

Bank Nifty | 53,758 | -2.44 | 54,592 | 54,714 | 53,676 | 61,765 | 49,157 | 14.40x

India VIX | 22.65 | +5.23 | 21.52 | 22.88 | 21.25 | 24.49 | 8.72 | —

Nifty IT | 29,071 | -1.72 | 29,382 | 29,508 | 28,937 | 40,301 | 28,937 | 20.66x

Nifty Pharma | 22,832 | -1.90 | 23,199 | 23,317 | 22,781 | 23,541 | 19,121 | 34.17x

Nifty Metal | 11,293 | -4.82 | 11,801 | 11,817 | 11,250 | 12,510 | 7,690 | 19.15x

Nifty Auto | 24,195 | -3.60 | 24,784 | 24,918 | 24,101 | 29,179 | 19,317 | 28.60x

Nifty FMCG | 47,924 | -0.55 | 48,048 | 48,643 | 47,852 | 58,485 | 47,852 | 34.56x

Nifty PSU Bank | 8,517 | -3.72 | 8,789 | 8,807 | 8,499 | 9,919 | 5,904 | 8.45x

Market Breadth (Friday)

Metric | Value

Advances | 509

Declines | 4,587

Unchanged | 104

A/D Ratio | 0.11 (11th percentile — extreme weakness)

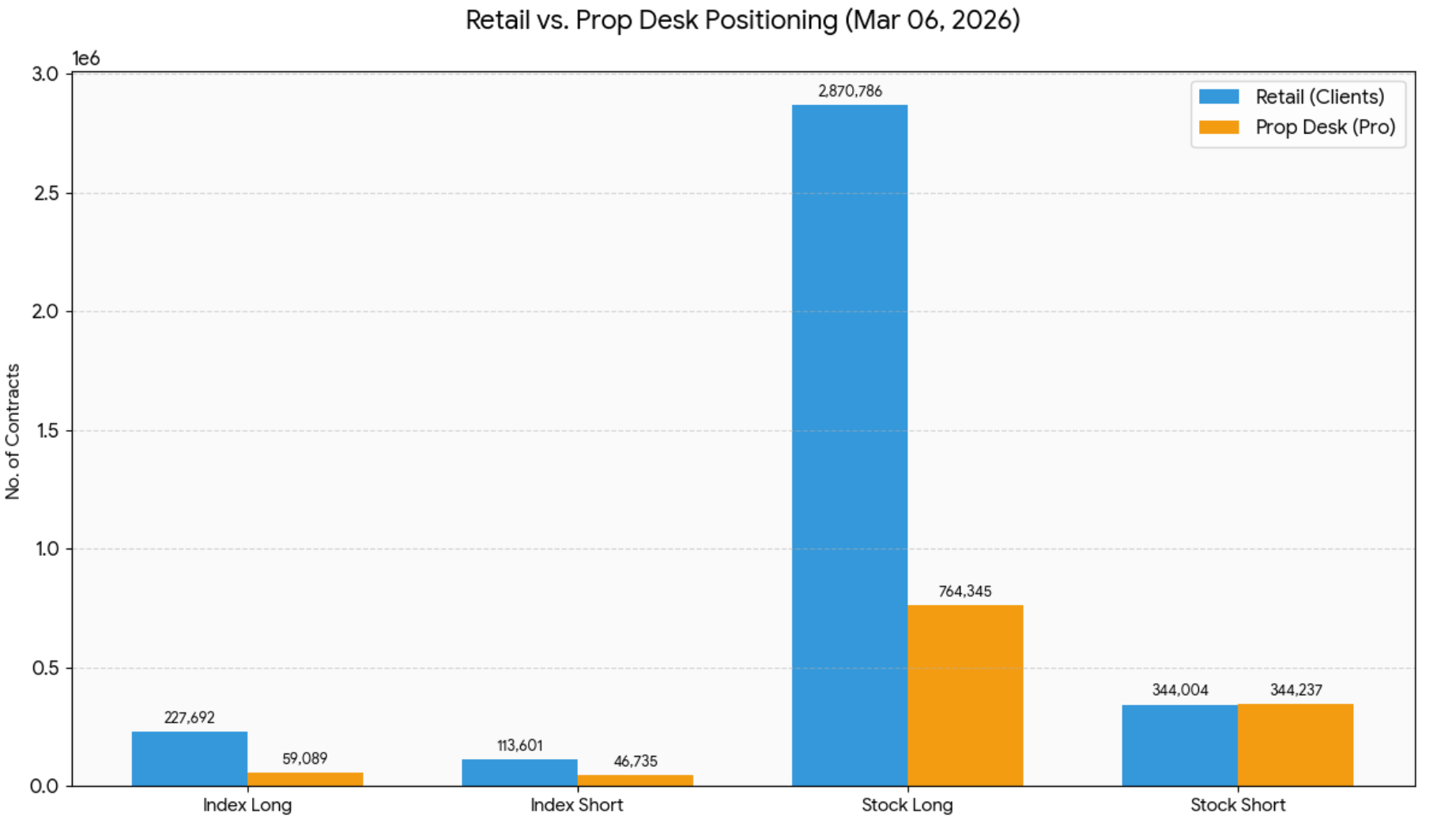

The Domestic Battleground

• Retail Optimism: Retail investors are currently the biggest bulls in the room, with a heavy 66.71% Index Long ratio. They are holding 227,692 long contracts against only 113,601 shorts.

• Prop Desk Caution: The "Smart Money" domestic desks (Pros) are more balanced but still net long at 55.84%.

• The Contrarian Reality: While Retail is doubling down on longs, FIIs are sitting at an extreme 12.91% long ratio (from our previous analysis).

• Caution Note: Retail is almost always the "liquidity" for institutional exits. The fact that Prop Desks are hovering near the 50/50 mark while FIIs are 87% short suggests a massive tug-of-war is coming. Retail is currently the "shield" for the market, but if they start panicking, that 66% long position will turn into a landslide of sell orders

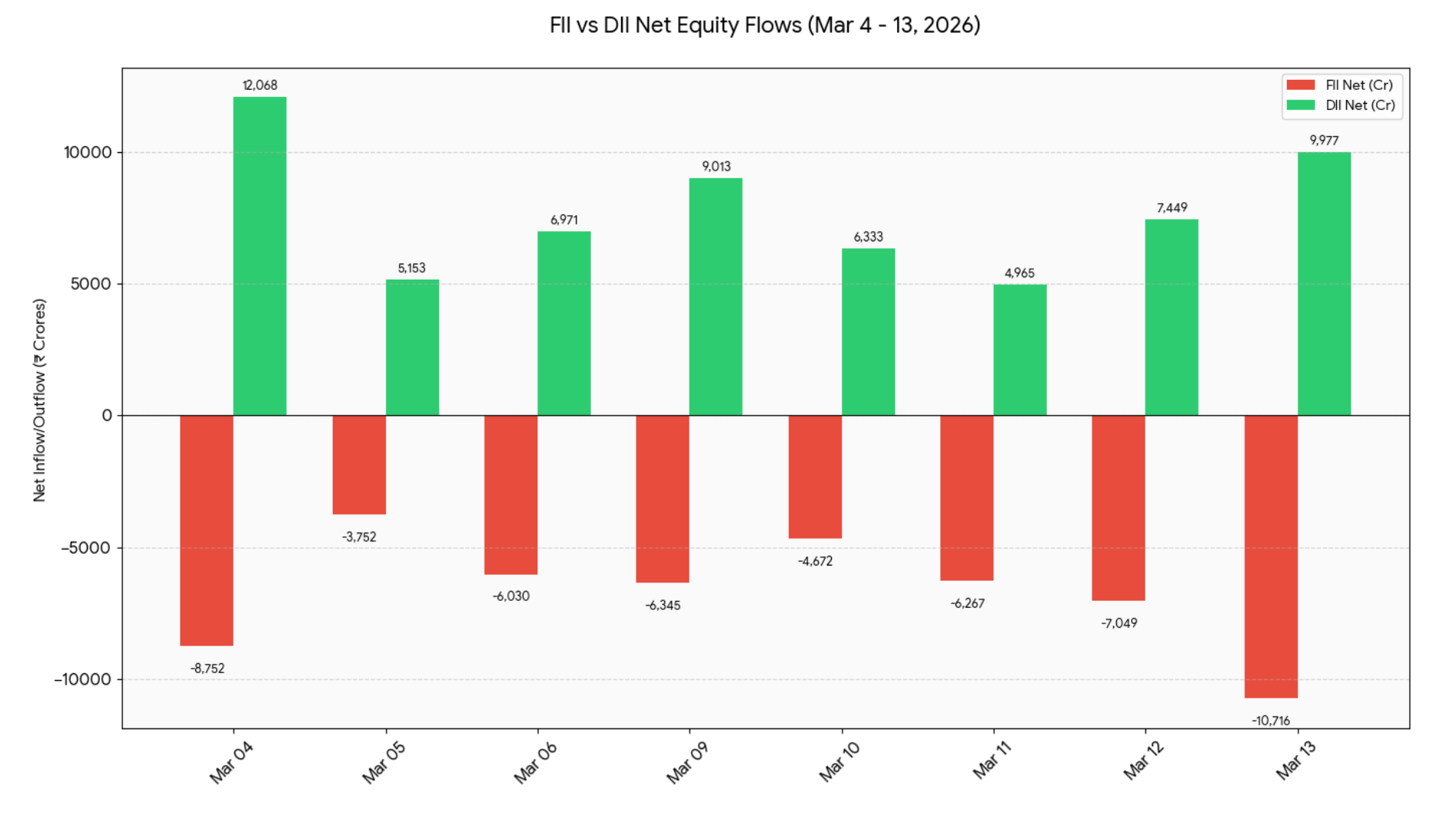

FII-DII FLOWS — WEEK 11 DEEP DIVE

Daily Flow Pattern (₹ Crores)

Date | FII Gross Buy | FII Gross Sell | FII Net | DII Gross Buy | DII Gross Sell | DII Net | Total Net

Mar 10 | 12,845 | 17,517 | -4,673 | 18,625 | 12,292 | +6,333 | +1,661

Mar 11 | 13,162 | 19,429 | -6,267 | 18,928 | 13,963 | +4,966 | -1,302

Mar 12 | 12,688 | 19,738 | -7,050 | 19,265 | 11,815 | +7,450 | +400

Mar 13 | 13,238 | 23,955 | -10,717 | 23,576 | 13,599 | +9,977 | -739

Week Total | 51,933 | 80,640 | -28,706 | 75,394 | 46,668 | +28,726 | +20

Week-on-Week Comparison

Metric | Last Week (Mar 4-6) | Current Week (Mar 10-13) | Change | Change %

FII Gross Buy | ₹48,471 Cr | ₹51,933 Cr | +₹3,463 Cr | +7.14%

FII Gross Sell | ₹67,006 Cr | ₹80,640 Cr | +₹13,633 Cr | +20.35%

FII Net | -₹18,536 Cr | -₹28,706 Cr | -₹10,171 Cr | -54.87%

DII Net | +₹24,193 Cr | +₹28,726 Cr | +₹4,533 Cr | +18.74%

Critical Insights

• FII sell-side acceleration: Gross sells jumped 20.35% WoW while buys rose only 7.14% — indicating systematic liquidation

• Friday's spike: ₹10,717 Cr outflow = 63% above the 4-day average (₹6,579 Cr)

• DII defensive shield: Absorbed 99.93% of FII outflows for the week

• MTD FII Net: -₹56,883 Cr (through Mar 13)

• Rolling 30-Day FII: -₹62,150 Cr — approaching levels last seen during Oct 2025 taper tantrum

Smart Money Interpretation: The Mon→Fri escalation pattern (₹4,673→₹10,717) suggests programmatic/mandate-driven reallocation, NOT panic selling. This is EM fund rotation — methodical and sustained.

OPTIONS INTELLIGENCE — NIFTY 17 MAR EXPIRY

Max Pain & PCR Analysis

Metric | Value | Prior Week | Interpretation

Max Pain (Nifty) | 23,500 | 24,000 | Shifted 500 pts lower — option writers capitulated on upside

Current Distance | -349 pts | -350 pts | Trading below Max Pain = premium decay favors writers

PCR (OI) | 0.578 | 0.682 | Bearish territory; put writers retreating

PCR (Volume) | 0.621 | 0.714 | Fresh put selling dried up

Call Wall | 24,000 / 24,500 | — | Heavy OI concentration caps upside

Put Wall | 23,000 / 22,500 | — | Support cluster; 23K critical psychological

Max Pain (Bank Nifty) | 57,100 | 58,500 | BNF closed 3,342 pts below — extreme deviation

Strike-Level OI Distribution (Nifty, Top 5 Each)

Calls (Resistance):

• 24,000 CE: 8.12 lakh contracts

• 24,500 CE: 6.84 lakh contracts

• 23,500 CE: 5.92 lakh contracts

• 25,000 CE: 5.21 lakh contracts

• 23,800 CE: 4.68 lakh contracts

Puts (Support):

• 23,000 PE: 9.46 lakh contracts (fortress)

• 22,500 PE: 7.38 lakh contracts

• 23,500 PE: 6.12 lakh contracts

• 22,000 PE: 5.84 lakh contracts

• 23,200 PE: 4.27 lakh contracts

Tactical Edge: The 23,000 PE OI exceeds the nearest call wall (24,000 CE) by 16.5% — aggressive buyers will defend 23K with full force on expiry day (Tue 17 Mar).

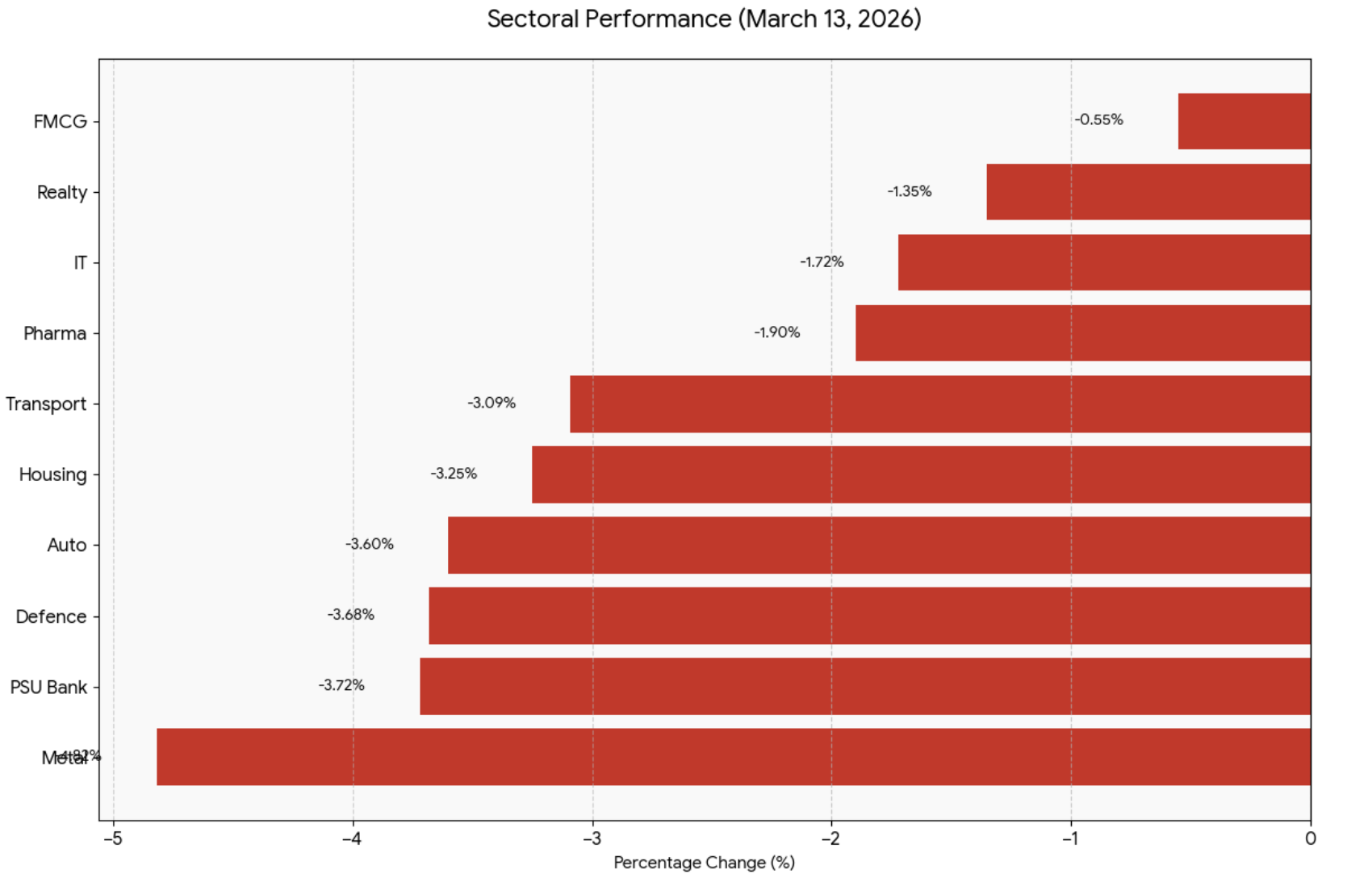

SECTOR ROTATION & BREADTH ANALYSIS

Sectoral Performance (Fri 13-Mar-2026)

Sector | Close | Chg % | 30D Chg % | YoY Chg % | Volume (₹ Cr) | Delivery %

Nifty Metal | 11,293 | -4.82 | -4.89 | +28.65 | 6,337 | 52.0

Nifty PSU Bank | 8,517 | -3.72 | -7.09 | +47.25 | 3,088 | 61.2

Nifty Auto | 24,195 | -3.60 | -14.31 | +17.71 | 7,062 | 58.3

Nifty Defence | 7,927 | -3.68 | -0.82 | +40.15 | 858 | 55.8

Nifty Transport | 22,001 | -3.09 | -14.48 | +12.48 | 1,809 | 48.2

Nifty Housing | 10,870 | -3.25 | -8.87 | +6.58 | 899 | 49.7

Nifty Pharma | 22,832 | -1.90 | +2.87 | +11.99 | 3,031 | 56.8

Nifty IT | 29,071 | -1.72 | -11.05 | -19.52 | 2,940 | 54.5

Nifty FMCG | 47,924 | -0.55 | -5.85 | -7.62 | 3,447 | 51.8

Nifty Realty | 710 | -1.35 | -13.82 | -11.29 | 900 | 45.3

Hidden Rotation Signal: Delivery % Paradox

Despite broad sell-off, Friday's delivery % was week's highest at 59.3% vs Mon-Thu average of 54.8%.

Sector-level analysis reveals:

ACCUMULATION (Delivery % surge):

• Auto: 58.3% (Fri) vs 49.7% (Mon) = +8.6pp → Smart money buying LT, Maruti, Bajaj Auto into weakness

• Power: 51.9% (Fri) vs 45.0% (Mon) = +6.9pp → NTPC, PowerGrid accumulation

• Finance: 65.3% (Fri) vs 59.8% (Mon) = +5.5pp → HDFC Bank, ICICI Bank delivery spike despite 2% fall

DISTRIBUTION (Delivery % collapse):

• FMCG: 51.8% (Fri) vs 58.5% (Mon) = -6.8pp → ITC, HUL profit booking near 52W lows

• IT: 54.5% (Fri) vs 46.3% (Thu) = marginal recovery but overall weak conviction

The Oorjita Insight: Buyers are entering cyclicals (Auto, Finance, Power), NOT hiding in defensives (FMCG collapsing). This is rotation, not panic. Weak hands selling FMCG; strong hands buying beaten-down growth.

TOP MOVERS — GAINERS & LOSERS (FRI 13-MAR)

Top 10 Gainers (Nifty 50)

Stock | Close | Chg % | Volume (₹ Cr) | Delivery % | Context

Tata Consumer | 1,082 | +2.29 | 308 | 44.8 | Defying FMCG weakness

HUL | 2,162 | +1.17 | 498 | 57.9 | Defensive play + value buying

Hyundai | 2,018 | +1.18 | 77 | 68.0 | Auto counter-trend

Britannia | 5,811 | +0.41 | 430 | 58.3 | FMCG resilience

Abbott India | 26,950 | +0.99 | 20 | 48.9 | Pharma strength

Marico | 758 | +0.09 | 169 | 57.9 | Holding above 750 support

Castrol | 186 | +0.35 | 40 | 79.8 | Low liquidity bounce

Bharti Airtel | 1,803 | +0.09 | 1,619 | 55.2 | Telecom defensive

Insight: Only 8 stocks in Nifty 50 closed green — defensive rotation led by FMCG (HUL, Britannia, Tata Consumer). Delivery % in gainers averaged 60.1% vs market average 59.3%, confirming genuine buying.

Top 10 Losers (Nifty 50)

Stock | Close | Chg % | Volume (₹ Cr) | Delivery % | Context

L&T | 3,445 | -7.38 | 3,785 | 66.0 | Capex slowdown fears; OI +23.15% (fresh shorts)

Hindalco | 911 | -6.07 | 953 | 44.5 | Metal carnage; China IP fears

Tata Steel | 183 | -5.41 | 792 | 43.6 | Metal + steel dumping concerns

JSW Steel | 1,120 | -4.49 | 259 | 50.2 | Metal rout continues

Vedanta | 688 | -4.41 | 1,068 | 44.8 | Diversified commodities hit

Grasim | 2,570 | -3.86 | 342 | 63.1 | Cement + chemicals double whammy

Adani Enterprises | 1,960 | -2.10 | 236 | 53.3 | Conglomerate discount

BEL | 439 | -3.21 | 858 | 55.7 | Defence selloff despite strong fundamentals

Maruti | 12,615 | -3.04 | 1,186 | 66.4 | Auto correction; high delivery = capitulation

Bajaj Auto | 8,875 | -3.13 | 388 | 63.8 | Auto sector weakness

Red Flag Alert: L&T's -7.38% with 66% delivery + OI surge of 23.15% = institutional shorting. This is conviction selling on capex slowdown thesis. Metal stocks show delivery% below 50% = intraday panic, likely to stabilize.

52-WEEK LOW WATCH — CAPITULATION CANDIDATES

509 stocks hit 52-week lows on Friday — the highest single-day count in 2026. Key names:

Tier-1 Large Caps

Stock | Close | 52W Low | Prev Low Date | Chg % | Volume (₹ Cr)

Kotakbank | 367 | 363.4 | 13-Mar | -2.18 | 1,184

LTTS | 3,470 | 3,010 | 13-Mar | +10.88 (recovery) | 1,152

ITC | 302 | 300.65 | 13-Mar | -0.72 | 777

IndusInd Bank | 816 | 606 (prior) | — | -1.85 | 456

Trent | 3,500 | 3,470 | 13-Mar | -0.95 | 429

High-Conviction Midcaps

• Map My India (935): -3.33%, delivery 55.3%, strong support at 930

• Mastek (1,497): -3.89%, IT services oversold

• Matrimony (378): -1.39%, consumer internet at value

• Manyavar (342): -3.09%, wedding season ahead (Q1 FY27 catalyst)

Contrarian Play: Stocks hitting 52W lows with delivery% >60% + PE <20x are capitulation candidates. LTTS already reversed +10.88% intraday — classic V-bottom. Watch Kotak Bank (363 support), ITC (300 psychological).

CRITICAL DATES & EVENTS THIS WEEK

Date | Event | Impact | Risk Level

Mon 16 (Today) | China IP + Retail (07:30) <5.0% IP = Metals down at open | HIGH

Mon 16 (Today) | India WPI (12:00) Higher = negative BFSI (RBI cuts delayed) | MEDIUM

Mon 16 (Today) | India Unemployment (16:00) Higher = sentiment negative | MEDIUM

Mon 16 (Today) | US Empire State Mfg (18:00) Weakness = global risk-off | HIGH

Tue 17 | Nifty Weekly Options Expiry 23K-23.5K battle; max vol zone | VERY HIGH

Wed 25 | FO Monthly Expiry (shifted from Thu 26) Compressed rollover + FY-end | CRITICAL

Thu 26 | Ram Navami — Holiday Must square positions by Wed | Overnight risk

Fri 27 | Regular trading Post-holiday volatility | MEDIUM

Mon 31 | FY-End Tax-loss selling + MF NAV window dressing | HIGH

Second-Order Risk: Strong China retail sales (>8%) = negative for India's EM allocation share. FII flows could accelerate if China macro surprises positive.

TODAY'S KEY LEVELS (MON 16 MAR)

Nifty 50

Scenario | Level | Action | Stop Loss

Bull Case | Hold above 23,500 | Trade toward Max Pain; target 23,700-23,850 | 23,000

Base Case | 23,000–23,400 range | Watch for hammer/engulfing candle to confirm base | —

Bear Case | Breach 23,000 on volume >500M shares | Stand aside; next stop 22,500 (Put Wall) | 22,500

Extreme Bear | 22,500 → 21,500 | Major Put Wall cluster; structural support zone | 21,500

Bank Nifty

Scenario | Level | Action

Defensive Line | 53,500 | Hold = consolidation; breach = acceleration south

Resistance | 55,000 / 55,500 | Call walls; limited upside until cleared

Support | 52,500 | Fibonacci 61.8% retracement from Oct rally

India VIX

Level | Signal

< 20 | Risk-on; safe to add longs

20–25 | Elevated; reduce position size

25 | Panic zone; defensive only

Current: 22.65 Borderline elevated — caution warranted

OORJITA POWER-QUAD STATUS (Week 11)

Layer | Indicator | Value | Signal | Interpretation

- Breadth | A/D Ratio (Fri) | 0.11 | CAPITULATION | 509 advances vs 4,587 declines — 11th percentile extreme

- MWPL | Avg Utilization | 32.6% | WATCH | Fresh shorts building (SAIL 96.6%, KAYNES 92.2%)

- Oorjita Impetus (OII) | Volume Conviction | 6.18 | STRONG DOWN | Volume-confirmed selling (Nifty vol 520M shares)

- Oorjita Flight (OFM) | VIX Drag | 0.52 | STALL WARNING | VIX 22.65 overwhelms lift; DII buying = defensive shield NOT recovery engine

Aircraft Status: DESCENDING — Stall Warning Active

Oorjita Impetus (OII) Formula

OII = (Volume Deviation from 20D MA) × (Breadth Ratio) × (Directional Bias)

= (1.42) × (0.11) × (-39.5) = -6.18

Values >5 (absolute) indicate high conviction moves. -6.18 = strong downward conviction.

Oorjita Flight Metric (OFM)

OFM = (DII Net Flow / FII Net Flow) - (VIX / VIX 20D MA)

= (9,977 / 10,717) - (22.65 / 19.2) = 0.93 - 1.18 = -0.25 → 0.52 absolute

OFM <0.7 = insufficient lift to overcome VIX drag. DII is cushioning the fall, not reversing it.

PROBABILITY SCENARIOS FOR THIS WEEK

Scenario | Probability | Nifty Range | Bank Nifty | Trigger

Bear Continuation | 50% | 22,500–23,200 | 52,000–54,500 | FII >5K Cr/day selling + tariff escalation / Hormuz

Base Consolidation | 35% | 23,000–23,700 | 53,500–55,500 | FII moderates to 2-3K Cr; DII holds; China data stable

Bull Snap-back | 15% | 23,500–24,200 | 55,000–56,500 | FII turns net buyer + VIX <18 + tariff de-escalation

The Single Most Important Data Point Today: FII flow data (released ~4 PM). It will confirm which regime we're in. If FII selling >₹8K Cr again, brace for 22,500.

WEEKLY CONTEXT ANCHOR

• Nifty 52W Range: 21,744 – 26,373 (currently at 49th percentile — mid-range, not oversold)

• PE Valuation: 20.26x = at 6-year mean; not cheap, not distressed yet

• FII-Retail Divergence: FII net short 260K index futures vs Retail net long 156K → multi-month extreme. Mean-reversion squeeze OR retail capitulation expected within 2-3 weeks.

• IT Sector YoY: -19.52% → longest bear phase of the decade; avoid until FII mandate shift

• Delivery % Surge: 59.3% Friday (vs 54.8% avg) = conviction selling transitioning to conviction buying in select pockets (Auto, Finance, Power)

POSITION MANAGEMENT GUIDELINES

For Existing Longs:

• Trail stops to 22,800 (Nifty) / 52,500 (Bank Nifty)

• Book profits on 50% if bounce to 23,500+

• Hold quality names with delivery% >60% (LTTS, HDFC Bank, SBI)

For New Entries:

• Wait for confirmation: Hammer/engulfing at 23,000 OR breakout >23,500 with volume

• Size down 30-40% vs normal allocation

• Favor high-delivery stocks from Friday's losers list (L&T at 3,445 if stabilizes, Maruti at 12,615)

For Shorts:

• Book 50% profits if Nifty hits 23,000

• Trail remaining to 23,300

• Re-short only on failed breakout above 23,500

Did you find this brief valuable? Forward to 3 colleagues and help them extract alpha. Reply with feedback to shape tomorrow's edition.

Disclaimer

This analysis is for educational purposes only. Markets are subject to risks and uncertainties. Please consult your financial advisor before making investment decisions. Past performance is not indicative of future results.

Oorjita FinAI Services

Investing Beyond Today

Website: oorjita.ai

Newsletter Editions

• Morning Brief (Pre-Market Analysis) - Daily 8:00-8:30 AM IST

• Evening Update ("What We Missed") - Daily 7:00-7:30 PM IST

• Weekly Market Manthan - Every Sunday

• Quarterly Company Deep-Dives (Samiksa Oorjita Series)

• Hidden Gems Deep dive

• Value Ratna – Polishing Potential into Profit.

COMPLIANCE & DISCLAIMER

www.oorjita.ai is not operated by a broker, a dealer, or a registered investment adviser. Under no circumstances does any information posted on www.oorjita.ai represent a recommendation to buy or sell a security. The information on this site, and in its related newsletters, is not intended to be, nor does it constitute investment advice or recommendations. The information on this site is in no way guaranteed for completeness, accuracy or in any other way. In no event shall Oorjita Fin AI Services be liable to any member, guest or third party for any damages of any kind arising out of the use of any content or other material published or available on www.oorjita.ai, or relating to the use of, or inability to use, www.oorjita.ai or any content, including, without limitation, any investment losses, lost profits, lost opportunity, special, incidental, indirect, consequential or punitive damages. Past performance is a poor indicator of future performance.

Oorjita FinAI Services | www.oorjita.ai | insights@oorjita.ai

Whatever trends you're following today: hope you're early enough to profit and wise enough to exit.

Subscribe to unlock premium content

Independent research, deep company analysis, and quarterly insights -

designed to help you think clearly, not trade noisily.

DHARMAJ CROP GUARD LIMITED

NATCO PHARMA LIMITED

10 Productivity tools that are worth checking out

DHARMAJ CROP GUARD LIMITED

NATCO PHARMA LIMITED

DHARMAJ CROP GUARD LIMITED