Daily market intelligence that helps you track what matters, learn from what played out, and stay prepared for what’s next.

Popular articles

Oorjita – Comprehensive Company Analysis

Dharmaj Crop Guard – Comprehensive Investment Analysis

Business Overview & Market Potential

Dharmaj Crop Guard (DCGL) manufactures agro-chemicals across branded formulations (B2C), institutional formulations (B2B domestic and exports), and active ingredients (AIs/technicals). The company operates within the Indian agrochemicals industry, which is expanding at a mid-to-high single-digit CAGR. India’s agrochemicals total addressable market (TAM) is estimated at ~US$9–13 billion, with additional global opportunities emerging as China+1 sourcing gains momentum.

Market Positioning

DCGL is a small- to mid-cap player relative to peers such as Rallis, Sumitomo Chemical India, and Sharda Cropchem. Its key differentiation lies in its branded B2C distribution reach (~18,000 retailers), growing institutional tie-ups, and ongoing AI capacity expansion.

Business Moats

The company’s primary moats include distribution scale, regulatory filings, and integration across active ingredients. While moat durability is currently moderate, it is improving as branded sales scale up and AI exports gain traction.

Moat Rating & Overall Score

Distribution: 6.5/10

Cost & Process Efficiency: 5.5/10

Regulatory Capability: 6/10

AI Integration: 6.5/10

Overall competitive-advantage score: 6.2/10

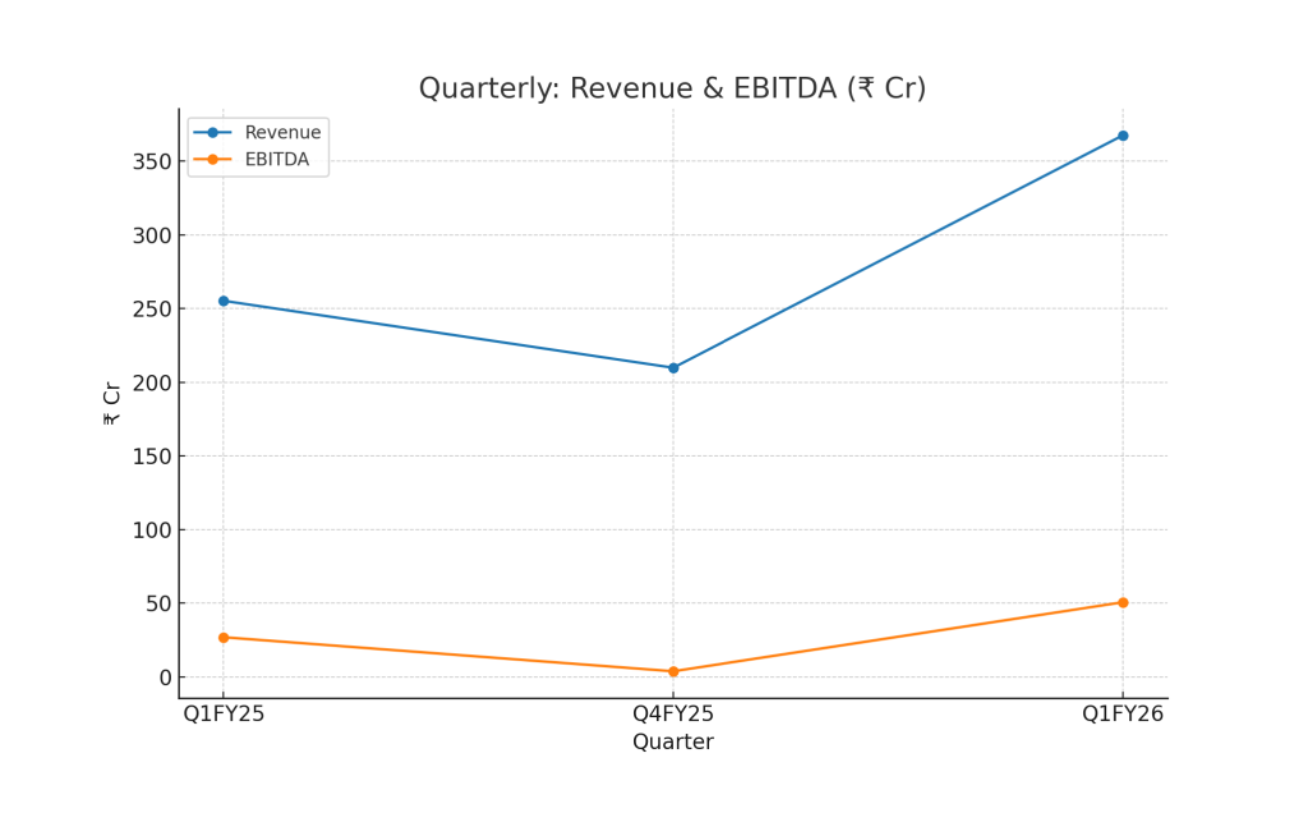

Quarterly Performance

In Q1 FY26, the company reported a strong rebound with revenue of ₹367 crore, EBITDA of ₹51 crore, and PAT of ₹33 crore, translating to EBITDA margins of 13.8%.

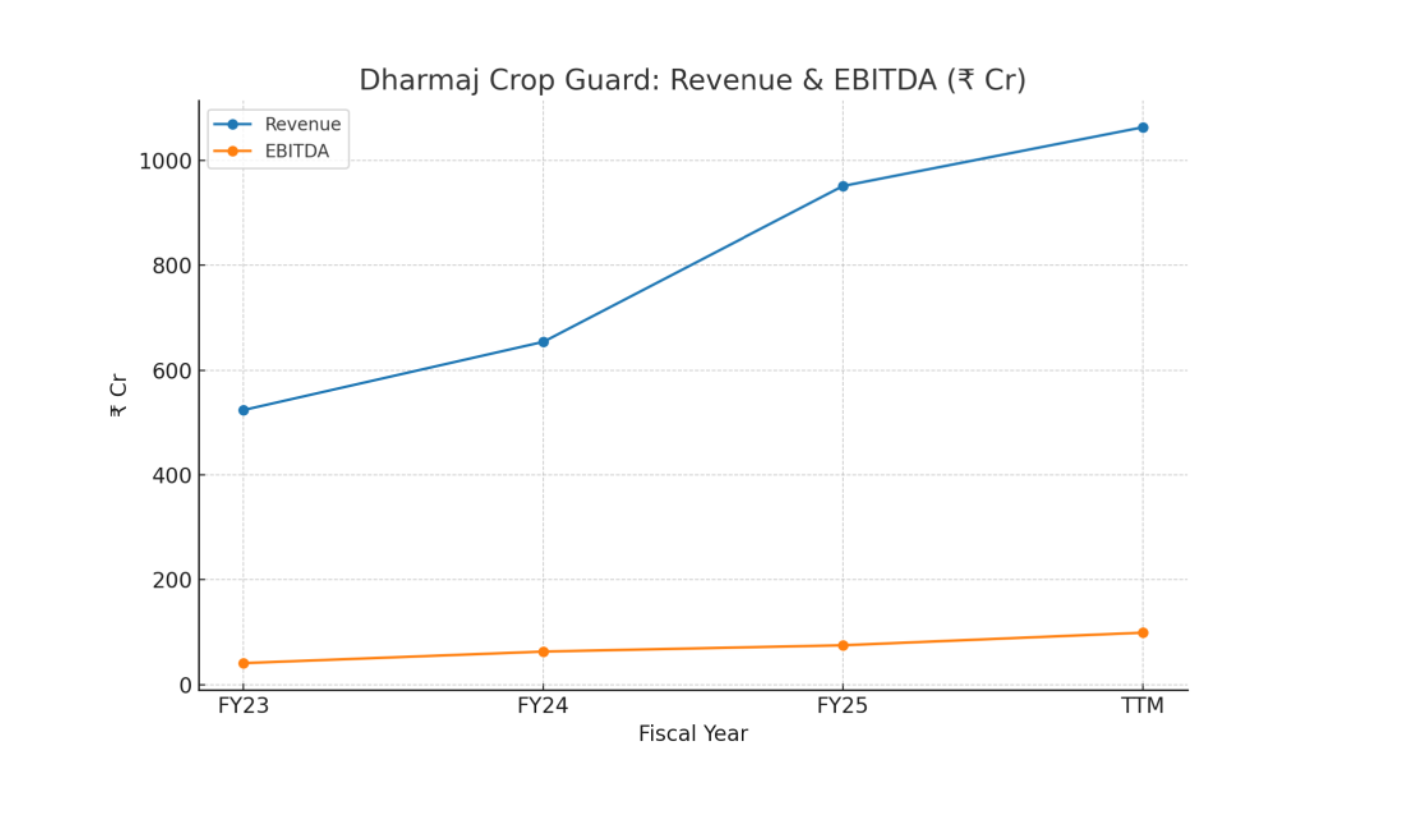

Annual Performance

Sales increased from ₹524 crore in FY23 to ₹951 crore in FY25, with EBITDA of ₹75 crore and PAT of ₹35 crore. Margins have remained volatile in the 8–10% range, but are showing signs of stabilization driven by higher AI contribution.

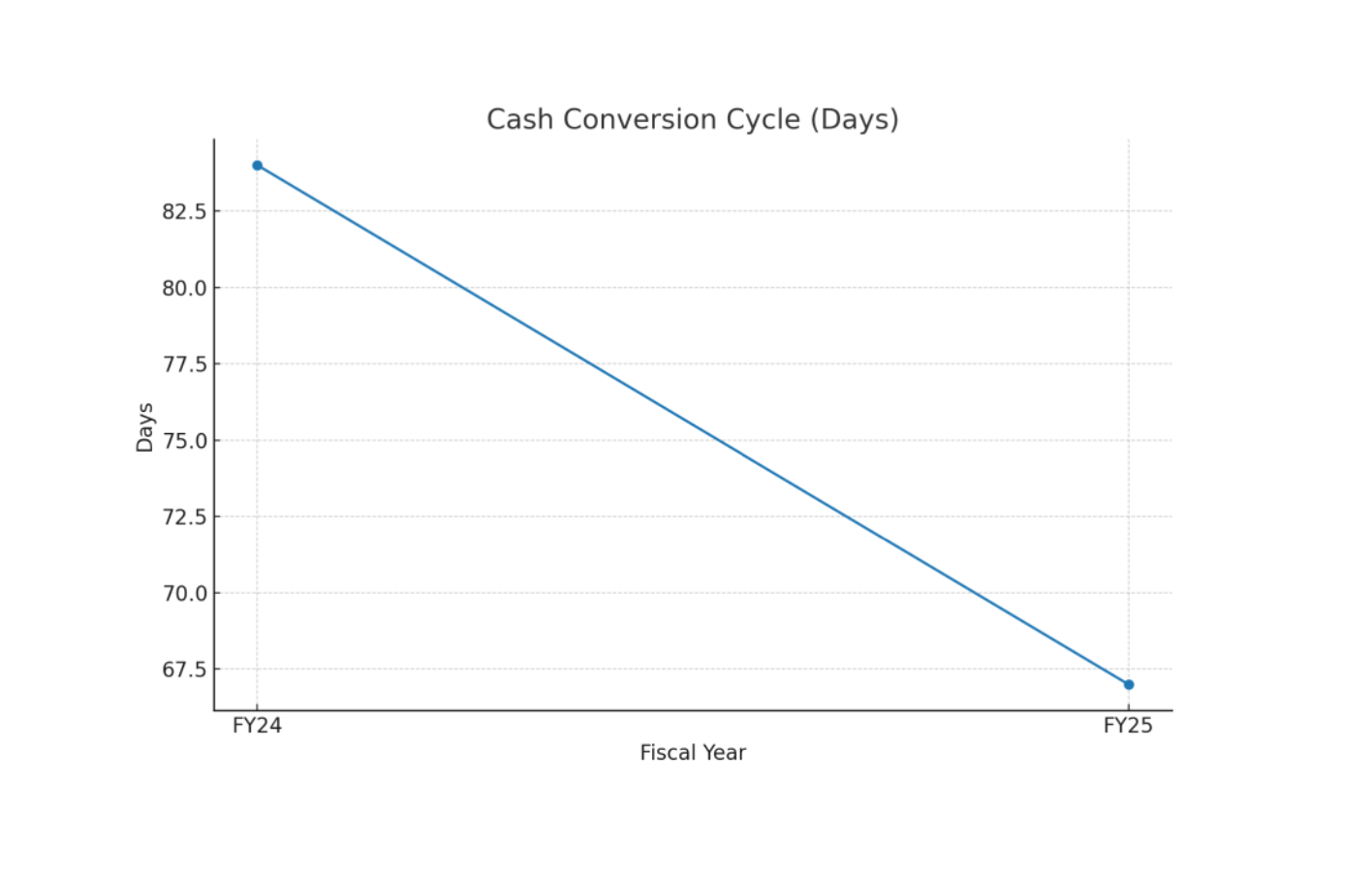

Working Capital & Cash Flow

Debtor days increased to 95 days in FY25 compared to 66 days in FY24. However, the cash conversion cycle (CCC) improved to 67 days from 84 days, primarily due to higher payables. Operating cash flows strengthened in FY25, with ₹39 crore generated from CFO.

Valuation Scenarios

- Base case fair value: ~₹470 per share

- Bear case: ~₹333 per share

- Bull case: ~₹641 per share

The stock is currently trading at ~₹351 per share.

Peer Comparison

On an EV/EBITDA basis, DCGL trades at ~13x, broadly in line with Rallis (13x) and India Pesticides (12x), at a premium to Sharda Cropchem (9x), and at a significant discount to Sumitomo Chemical India (42x).

Investment Thesis & Action Points

- Closely monitor debtor days, especially receivables exceeding 180 days.

- Track AI capacity utilization and recovery in export demand.

- Watch the branded B2C ramp-up and its impact on margins.

- Valuation appears attractive, offering 30–35% upside under the base-case scenario.

Titikṣā in gains; Upekṣā in exits.

Subscribe to unlock premium content

Independent research, deep company analysis, and quarterly insights -

designed to help you think clearly, not trade noisily.

DHARMAJ CROP GUARD LIMITED

NATCO PHARMA LIMITED

10 Productivity tools that are worth checking out

DHARMAJ CROP GUARD LIMITED

NATCO PHARMA LIMITED

DHARMAJ CROP GUARD LIMITED